Online Casino Fees & Transaction Charges: What You Might Pay (and How to Avoid Them)

Online casinos can charge fees every time you move money. Deposits, withdrawals, currency exchange, and even inactivity can add extra costs. These charges often come from payment providers, banks, card networks, or the casino itself. They cut into your bankroll and slow down cashouts.

This guide breaks down the main fee types, where they show up, and what they usually look like in real terms. You will learn how to spot fee traps in the cashier and terms, pick payment methods with lower costs, avoid conversion markups, and reduce delays that lead to extra checks. You will also learn why matching your deposit and withdrawal method matters, and how faster identity verification can help you avoid failed withdrawals and repeat processing.

Key Takeaways

- In het kort: Check the cashier before you deposit. Look for fees by method, currency, and withdrawal limits.

- In het kort: Expect the main costs to come from bank transfer fees, card cash-advance fees, and currency conversion markups.

- In het kort: Use one method for both deposit and withdrawal. Mismatches often trigger extra checks, delays, or forced method changes.

- In het kort: Avoid currency conversion where you can. Use the casino account currency that matches your card or e-wallet, or a provider with low FX.

- In het kort: Watch withdrawal rules. Some casinos charge per withdrawal, set minimums, or limit free withdrawals per month.

- In het kort: Verify your identity early. Fast KYC reduces failed withdrawals and repeat processing.

- In het kort: Read bonus terms for payment limits. Some bonuses block certain methods or cap withdrawals unless you use an approved method.

- In het kort: Track the full cost. Add casino fees, payment provider fees, and FX spread to see what you really pay.

- In het kort: Keep deposit steps clean. Use a method with clear pricing, then follow a simple deposit flow to avoid errors and reversals.

Use the same payment method for deposit and withdrawal, match your account currency to your funding currency, and complete KYC before your first cashout. If you need a quick refresher on the deposit flow, follow our step-by-step deposit guide.

What online casino fees and transaction charges are (and who charges them)

A quick definition, fees vs. limits vs. delays

Fees are extra costs taken from your deposit, your withdrawal, or your balance. They show up as a fixed charge, a percentage, or a worse exchange rate.

Limits are caps on how much you can deposit or withdraw per transaction, per day, or per month. Limits can force you to split cashouts, which can trigger multiple fees.

Delays are time, not money. They include processing windows, pending statuses, and compliance checks. Delays can lead to extra costs if they cause reversals or repeated attempts.

The four main fee sources

- The casino. Sets its own fee policy for deposits, withdrawals, inactivity, and sometimes specific payment rails. Some casinos also add handling fees for certain currencies or low cashout amounts.

- The payment processor. This includes card networks, e-wallets, prepaid voucher issuers, and crypto gateways. They can charge top-up fees, withdrawal fees, or conversion fees inside their app.

- Your bank and intermediaries. Banks can charge wire fees, international transfer fees, and incoming payment fees. Intermediary banks can deduct charges mid-transfer, so the casino receives less than you sent.

- Currency exchange. FX fees come from the casino, your bank, your card issuer, or your wallet. You pay via a marked-up rate, not a line-item fee. You often miss it because it looks like normal conversion.

Where fees show up in your journey

- Deposit. Card funding fees, wallet top-up fees, instant bank transfer fees, or crypto network fees. Some casinos charge a deposit fee only for specific methods or small deposits.

- Play. Most casinos do not charge a fee to place bets. Costs can still appear through currency conversion if the game wallet runs in a different currency than your deposit.

- Bonus use. You can pay indirectly through wagering rules. Some casinos also exclude certain games or bet sizes, which can slow clearance and increase the chance you hit an inactivity rule before you cash out.

- Withdrawal. The most common fee point. You can see fixed cashout fees, percentage fees, bank receiving fees, and FX spread if the cashout currency differs. Some methods also force a minimum cashout, which can make small withdrawals inefficient.

- Inactivity. A monthly fee after a defined idle period. It reduces your balance until you log in, resume play, or your balance hits zero.

Why fee disclosures can be confusing

- Cashier pages often show only casino-side fees. Processor fees and FX markup can sit outside the casino checkout flow.

- Fees hide inside exchange rates. The page may say “0% fees” while you still lose value on conversion.

- Different rules for deposit and withdrawal. A method can be free to deposit and expensive to withdraw, or not supported for withdrawal at all.

- Tiered pricing. Fees can change by country, currency, VIP level, or withdrawal size. You see the real cost only after you enter an amount.

- Terms split across pages. The cashier, banking FAQ, and bonus terms can each contain fee-related rules. You need to check all three before you assume a method is “free”.

- Pending and reversal events. A failed cashout can lead to repeated attempts, extra conversion, or extra bank charges. If your withdrawal sits in review, use this guide on why withdrawals go pending.

Common fee types you may pay at online casinos

Deposit fees, when “free deposits” is not truly free

Many casinos list deposits as “free” because they do not add a cashier fee. You can still pay charges through your payment provider, your bank, or the exchange rate.

- Card processing and issuer charges. Your bank can treat a casino deposit as a cash-like transaction and add a fee and interest.

- Minimum deposit traps. A method can look fee-free but force a higher minimum. You fund more than you planned to avoid a decline.

- FX baked into the rate. You deposit in one currency, the casino credits another, you pay the spread even if the cashier shows “0 fee”.

- Third-party wallet funding fees. Some e-wallets charge to load via card, then the casino deposit itself shows as free.

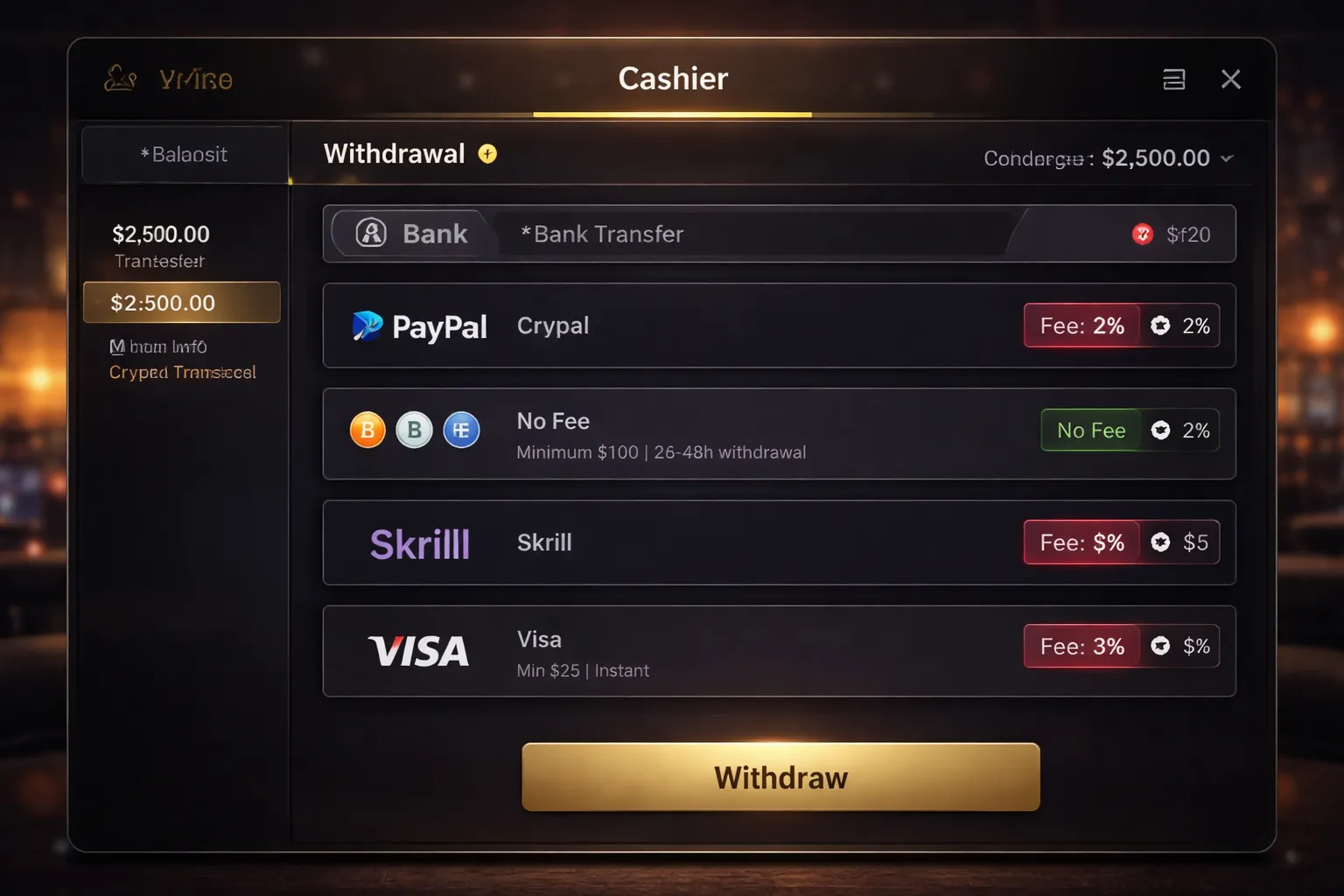

Withdrawal fees, flat fees, percentage fees, and tiered schedules

Withdrawal fees hit harder than deposit fees because you pay them when you try to take money out. Casinos usually apply them per cashout, not per day.

- Flat fee. A fixed amount per withdrawal. Example, $5 per cashout.

- Percentage fee. A cut of the amount. Example, 2% of $500 equals $10.

- Tiered schedules. Fee depends on size or method. Example, free above $200, $10 below $200.

- Free withdrawals with limits. Some casinos give 1 to 3 free cashouts per month, then charge after that.

- Method switching fees. If you deposit with one method and withdraw with another, the casino can add a manual processing fee or refuse the cashout.

Currency conversion (FX) charges and dynamic currency conversion pitfalls

FX costs often beat visible fees. You pay them through a conversion fee, a poor exchange rate, or both.

- Casino-side conversion. The casino converts your deposit or withdrawal and adds a percentage fee, or uses a marked-up rate.

- Provider-side conversion. Your card, bank, or wallet converts and adds its own spread.

- Double conversion. You deposit in USD, the casino account runs in EUR, then your bank posts the transaction in GBP. Each step can add a spread.

- Dynamic currency conversion (DCC). Some processors push you to accept conversion “for your convenience” at checkout. You usually get a worse rate than your card network rate. Choose to pay in the original currency when you can.

Bank and card issuer fees, cash advance, gambling blocks, and international charges

Your casino can charge zero and you still pay your bank. These charges show on your statement, not in the casino cashier.

- Cash advance fees and interest. Some issuers code gambling deposits as cash-like. You can pay an upfront fee and immediate interest with no grace period.

- International transaction fees. If the casino processor sits overseas, your bank can add a foreign transaction fee, even if the casino displays your local currency.

- Gambling blocks and declines. Blocks can trigger failed deposits. Repeated attempts can cause holds, reversal delays, or multiple small bank fees.

- Intermediary bank fees. Bank wire withdrawals can lose money to correspondent banks on the way to you.

E-wallet and prepaid voucher charges, loading, transfer, and withdrawal costs

Wallets and vouchers can reduce banking friction, but they can add their own fees at each step.

- Load fees. Funding a wallet with a card can cost more than funding by bank transfer.

- Transfer fees. Some wallets charge to send money out, convert currency, or move funds between users.

- Wallet withdrawal fees. Pulling money from the wallet to your bank account can cost a flat fee or a percentage.

- Voucher costs. Vouchers often include a purchase markup at the retail point, plus limits that force multiple purchases.

- Voucher withdrawal limits. Many casinos do not allow withdrawals back to vouchers. You may need to add a bank or wallet, which can trigger extra checks and new fees.

Inactivity, dormancy, and account maintenance fees

Some casinos charge you when you stop playing. Terms usually define inactivity as no login, no bets, or no transactions for a set period.

- Inactivity fees. A monthly deduction after a set number of inactive months.

- Dormancy escalation. Fees can rise after longer periods, or the casino can close the account and deduct an admin charge.

- Balance targeting. Fees typically deduct from your cash balance first, not from bonus funds.

Chargeback and dispute-related fees (and when they apply)

Chargebacks cost casinos money. Some pass that cost to you when they believe you misused the dispute process or broke payment rules.

- Chargeback handling fee. A fixed amount added if you file a chargeback after accepting the casino’s terms, or after a withdrawal paid to you.

- Collection and admin fees. If a chargeback reverses funds you already wagered, the casino can treat it as a debt and add admin costs.

- Account restrictions. Casinos often lock withdrawals and bonuses during disputes. Fees can follow if your account enters a negative balance.

Bonus-related costs, wagering requirements, max cashout rules, and forfeiture triggers

Bonuses rarely add a visible “fee”. They add conditions that can reduce what you can withdraw, or force you to forfeit winnings.

- Wagering requirements. You must stake a multiple of the bonus, or bonus plus deposit, before you can withdraw. This increases expected losses and time at risk.

- Max cashout caps. Some bonuses limit withdrawals to a fixed amount or a multiple of the bonus. Any excess winnings get removed.

- Max bet rules. Betting over the limit during wagering can void the bonus and related winnings.

- Game weighting. Slots may count 100% toward wagering, table games may count 0% to 20%. You can waste bankroll clearing wagering on low-contribution games.

- Time limits. If you miss the deadline, the casino can cancel the bonus and any linked winnings.

- Withdrawal triggers forfeiture. Some casinos remove the bonus and winnings if you request a withdrawal before you complete wagering.

- Withdrawal limits stack with bonus terms. A low cashout cap can force multiple withdrawals and multiply per-withdrawal fees. See withdrawal limits rules that can create this problem.

Payment methods compared: likely charges, speed, and best use cases

Payment methods compared: likely charges, speed, and best use cases

| Method | Likely charges you may face | Typical deposit speed | Typical withdrawal speed | Best use cases |

|---|---|---|---|---|

| Credit and debit cards (Visa, Mastercard) | Casino deposit fee possible. Bank cash-advance fee and interest possible. FX fee on cross-border payments. | Instant | 1 to 7 business days | Fast deposits. Simple setup. Good if your bank does not treat it as cash. |

| Bank transfer, instant banking | Bank wire fee possible. Intermediary bank fee possible. FX spread on international transfers. Instant banking provider fee possible. | Instant to 2 business days | 1 to 5 business days | Large amounts. Lower fee risk than cards for some players. Strong for withdrawals if supported. |

| E-wallets (PayPal, Skrill, Neteller) | Wallet funding fees possible. Wallet FX fees are common. Withdrawal or transfer-out fees may apply. | Instant | Instant to 24 hours, then bank cashout adds time | Fast cashouts. Privacy from card statements. Good if the casino supports wallet withdrawals. |

| Prepaid cards and vouchers (PaysafeCard) | Voucher purchase markup possible. Currency conversion costs. Account fees possible if you use a wallet-linked version. | Instant | Often not available | Deposit-only control. Budgeting. Good if you want to avoid sharing bank data. |

| Crypto payments | Network or gas fees. Exchange fees. Spread on conversion. Volatility can change your real cost. | Minutes to 1 hour | Minutes to 24 hours, plus network confirmations | Borderless payments. Fast processing. Useful when cards and banks fail. |

| Mobile payments (carrier billing, mobile wallets) | Carrier surcharge possible. Higher effective fees via marked-up pricing. Wallet FX and top-up fees possible. | Instant | Often limited or not available | Small deposits. Convenience. Good when you do not want to use a card online. |

Credit and debit cards (Visa, Mastercard): when card deposits become expensive

- Cash-advance treatment. Some banks code gambling deposits as cash-like transactions. You can pay a cash-advance fee and immediate interest.

- Cross-border costs. If the casino merchant sits in another country, your bank may add FX and international processing fees.

- Multiple small deposits. Flat bank fees and casino deposit fees hurt more when you split deposits.

- Chargeback risk. Disputes can freeze your account. A freeze can delay withdrawals and increase the chance you hit time limits on bonuses.

Best move: use cards for deposits only if your bank treats them as standard purchases. Keep deposits fewer and larger. Avoid cards for withdrawals if the casino pushes you to a different method later.

Bank transfer and instant banking: fee risks and processing timelines

- Wire and intermediary fees. International transfers can pick up extra charges in the middle. You see less money arrive than you sent.

- Instant banking provider fees. Some open-banking style tools charge a small fee or bake cost into FX.

- Timeline reality. Deposits can be instant with instant banking. Classic transfers can take 1 to 2 business days. Withdrawals often take 1 to 5 business days after approval.

- Reconciliation delays. If your transfer reference is wrong, the casino can delay crediting your account.

Best move: use bank methods for larger deposits and for steady withdrawals. Match the account name to your casino profile. Save proof of payment.

E-wallets (PayPal, Skrill, Neteller): convenience vs. provider-side charges

- Fast cashouts. Many casinos process wallet withdrawals faster than cards and bank transfers.

- Wallet fees sit outside the casino. You can pay to fund the wallet, convert currency, or withdraw from the wallet to your bank.

- FX is the common leak. If your wallet balance currency does not match the casino currency, conversion adds cost each time.

- Withdrawal matching rules. Some casinos require you to withdraw to the same wallet you used to deposit. If you used a different method, you may face extra steps or delays.

Best move: keep one main wallet per casino. Hold the same currency in your wallet as your casino account when possible. Check wallet cashout fees before you choose it for withdrawals.

Prepaid cards and vouchers (PaysafeCard): where fees and limits typically bite

- Deposit-only problem. Many casinos do not pay winnings back to vouchers. You must add a bank account or e-wallet for withdrawals.

- Voucher limits. Per-voucher and per-transaction caps can force you to use multiple codes, which can create more friction and more failed deposits.

- FX and local pricing. You can lose value if the voucher currency does not match your casino currency.

- Account-related charges. Some prepaid ecosystems add account maintenance fees or cashout fees once you move beyond vouchers.

Best move: use vouchers for controlled deposits. Set up your withdrawal method first so you do not get stuck later. If your casino has low withdrawal caps, voucher deposits can make multi-withdrawal plans harder.

Crypto payments: network fees, spreads, and volatility considerations

- Network and gas fees. Fees change with congestion. A small withdrawal can become expensive on high-fee networks.

- Exchange spread. You often pay more in the buy and sell price than you see in a posted fee.

- Volatility. Your balance can drop between deposit and withdrawal even if you do not play. Stablecoins reduce this risk but do not remove fees.

- Confirmation times. Casinos may wait for multiple confirmations. That adds minutes or longer during peak traffic.

Best move: pick lower-fee networks when the casino supports them. Avoid frequent small transfers. Track the full path cost, exchange fee plus spread plus network fee.

Mobile payment options: carrier rules, limits, and potential surcharges

- Carrier billing costs. Some carriers add a surcharge or treat it like premium billing. You can pay more than the face value of the deposit.

- Low limits. Daily and monthly caps are common. You can hit limits fast and end up switching methods mid-bonus.

- Withdrawals often fail here. Many casinos do not withdraw to carrier billing. You need a second method for cashouts.

- Wallet top-up fees. If you use a mobile wallet that you top up by card, you can stack card fees and wallet fees.

Best move: use mobile methods for small, one-off deposits. Do not rely on them for withdrawals. Decide your withdrawal rail before you deposit.

For a deeper breakdown of fees, speed, and limits across providers, see online casino payment methods compared.

How casinos calculate and apply charges (with real-world scenarios)

Flat fee vs. percentage fee

Casinos usually charge one of two ways. A flat fee per withdrawal, or a percentage of the amount.

Flat fees punish small cashouts. Percentage fees punish big cashouts.

| Fee type | Rule | $100 withdrawal | $1,000 withdrawal |

|---|---|---|---|

| Flat | $5 per withdrawal | $5 (5%) | $5 (0.5%) |

| Percentage | 2.5% of amount | $2.50 | $25 |

Best move: if you face a flat fee, withdraw less often. If you face a percentage fee, avoid large one-shot withdrawals when you can split them without triggering extra flat charges or limits.

Minimum and maximum withdrawal limits create hidden costs

Limits change your fee math. They can force extra transactions.

- Minimum withdrawal. If the casino sets a $50 minimum and you have $42, you either keep playing, add funds, or wait. Each option can cost you more in fees or losses.

- Maximum per withdrawal. If the casino caps a withdrawal at $2,000 and you want $6,000, you need three withdrawals. If each withdrawal has a fee, you pay it three times.

- Daily or weekly caps. Caps can push withdrawals into multiple days. That can add bank charges, FX swings, and more opportunities for intermediary deductions.

Check caps before you deposit, especially if you plan to cash out a big win. Use withdrawal limits explained to map daily, weekly, and monthly ceilings.

Multiple small withdrawals vs. one larger withdrawal

Small withdrawals feel safer. Fees often make them expensive.

| Scenario | Withdrawal plan | Total fees | Net received |

|---|---|---|---|

| Flat fee | 4 withdrawals of $250, $5 each | $20 | $980 |

| Flat fee | 1 withdrawal of $1,000, $5 each | $5 | $995 |

| Percentage fee | 4 withdrawals of $250, 2.5% each | $25 | $975 |

| Percentage fee | 1 withdrawal of $1,000, 2.5% each | $25 | $975 |

Takeaway: flat fees reward fewer withdrawals. Percentage fees make the count irrelevant, but limits and fixed bank charges can still make extra withdrawals cost more.

FX plus withdrawal fee stacking

Double charging happens when you combine currency conversion with a withdrawal fee.

Real-world scenario:

- You play in EUR. Your bank account runs in USD.

- The casino charges a 2% FX margin to convert EUR to USD.

- Your withdrawal method charges a $10 withdrawal fee.

| Item | Amount |

|---|---|

| Withdrawal request | $1,000 |

| Casino FX margin (2%) | -$20 |

| Withdrawal fee (fixed) | -$10 |

| Net received | $970 |

Best move: pick a casino account currency that matches your withdrawal destination. If you must convert, convert once, at the cheapest rail, not twice across casino and wallet or bank.

Weekend and holiday processing and intermediary deductions

Casinos often “process” withdrawals fast, then banks and networks move the money on business days.

- Timing risk. A Friday night cashout can sit until Monday. If FX applies at settlement, your rate can change.

- Intermediary banks. International wires can route through one or more banks. Each bank can take a handling fee before the money reaches you.

- Shared fees. Some transfers use “SHA” fee mode. You and the recipient bank split charges, so you receive less than the amount sent.

If you need predictable net amounts, avoid wires for small to mid-size withdrawals. Use rails that show fees upfront and settle with fewer middlemen.

When casinos pass on third-party costs vs. absorbing them

Casinos decide who pays. Sometimes you pay. Sometimes the casino pays, but only under conditions.

- Pass-through model. The casino charges you whatever the provider charges them. You see it as a withdrawal fee, a bank fee, or a “handling” fee.

- Absorb model. The casino covers routine fees, but may limit free withdrawals per month, cap free amounts, or restrict free withdrawals to certain methods.

- Threshold model. The casino waives fees above a certain withdrawal amount, or only for VIP tiers.

- Exception model. The casino covers local transfers but charges for international payments, FX conversions, or manual processing.

Read the cashier screen before you confirm. If the casino does not show a clear net amount, assume extra charges can hit after the money leaves the casino.

Where to find fee information before you deposit

Cashier page checks, icons, tooltips, and method notes

Start in the cashier, before you enter an amount.

- Look for fee labels. Check for “fee”, “charge”, “commission”, “service fee”, “processing fee”, “FX”, “conversion”, or “network fee”.

- Open every tooltip icon. Casinos often hide method rules behind small “i” icons, question marks, or dropdown arrows.

- Check method specific notes. Many sites show different terms for cards, e wallets, crypto, and bank transfer. Read the note shown under the method name, not the general cashier header.

- Check the net amount. If the cashier shows only the deposit amount, but not the received amount, treat it as a warning sign.

- Check the withdrawal tab too. Fees often show only on withdrawals, or only after you switch from “Deposit” to “Withdraw”.

- Check limits and processing options. “Manual review”, “priority”, or “instant” options can add a fixed fee.

Terms and Conditions sections that often contain fee clauses

Use the site search in your browser. Scan for specific words. Do not skim the full document.

- Banking or payments terms. Look for sections named “Payments”, “Deposits”, “Withdrawals”, “Cashier”, or “Financial transactions”.

- Fee triggers. Look for clauses tied to “chargeback”, “returned payment”, “failed withdrawal”, “reversed transfer”, or “incorrect details”.

- Inactivity and account maintenance. These fees do not appear in the cashier, but they reduce your balance over time.

- Currency and conversion rules. Search “base currency”, “exchange rate”, “FX”, “conversion”, “DCC”, or “spread”.

- Extra verification and compliance. Search “KYC”, “source of funds”, “enhanced due diligence”, or “manual processing”. Some sites reserve the right to charge for special handling.

- Withdrawal frequency rules. Search “one free withdrawal”, “monthly”, “weekly”, “per 24 hours”, or “subsequent withdrawals”. These lines often hide the real cost.

Banking and payments pages, site wide rules vs method specific rules

Many casinos split the rules. One page covers the general policy. Another page covers each payment method.

- Site wide rules. These include payout schedules, verification requirements, withdrawal limits, and fee models like “one free per month”. They can apply even if a method page shows “0%”.

- Method specific rules. These include network fees for crypto, card processing fees, local transfer coverage, and supported currencies. They can override the general page for that method.

- Match the method you will use. If you plan to deposit by card and withdraw by bank transfer, read both sets of rules. Do not assume the same fee policy applies.

- Compare methods before you pick one. Use this guide on online casino payment methods to check common fee patterns by payment type.

VIP and loyalty pages, fee waivers and faster withdrawals

VIP tiers often change your real cost.

- Fee waivers. Look for “free withdrawals”, “fees covered”, or “bank fees reimbursed”. Check if the waiver covers all methods or only bank transfer.

- Withdrawal frequency. Some tiers give more free withdrawals per week or per month, then charge for extra requests.

- Priority processing. Faster approvals reduce the risk of intermediary bank fees on repeated attempts, but some casinos charge for “express” handling.

- Eligibility rules. Check if the tier requires a minimum deposit, wagering, or a rolling period. A waiver that you cannot keep does not help.

Customer support questions to confirm your total cost

Ask for numbers and conditions. Save the reply.

- “What is the total fee for this deposit method, including any processor or network fee?”

- “If I withdraw $X, what amount will leave the casino, and what amount should reach my wallet or bank?”

- “Do you charge for more than one withdrawal per day, week, or month?”

- “Do you charge extra for manual review, enhanced checks, or failed withdrawals?”

- “Do you apply currency conversion, and what rate source do you use?”

- “If an intermediary bank deducts fees, do you reimburse them, and in what cases?”

- “Where in your Terms does it state this fee rule?” Ask for the exact section name.

How to avoid or reduce online casino fees and transaction charges

Pick fee-light methods

Your payment method sets your baseline costs. Start with methods that usually carry the lowest fee load at the casino side.

- Bank transfer where supported, often low or zero casino fees, but your bank or an intermediary bank can still deduct a charge.

- Debit card, often cheaper than credit, but some casinos add a fixed withdrawal fee or limit free withdrawals.

- E-wallets, usually fast and reliable, but you may pay provider fees when you move money from the wallet to your bank or when you convert currency.

- Prepaid vouchers, good for deposits, weak for withdrawals. You often must withdraw via bank or another method, which can trigger extra checks and delays.

- Crypto, can reduce banking fees, but you still face network fees and price movement risk. Some casinos also add their own crypto withdrawal fee.

Use the same method for deposits and withdrawals

Match your deposit method to your withdrawal method wherever the casino allows it. Casinos run source-of-funds and anti-fraud checks. A mismatched method can trigger manual review, extra documents, or a rejected payout that you must resubmit.

- Deposit with the method you want to withdraw to.

- Avoid mixing cards, vouchers, and multiple wallets unless you must.

- If you changed banks or cards, update details before you request a withdrawal.

Stay in one currency

Currency conversion is one of the most common silent costs. You pay it when your bank, card network, wallet, or the casino converts money at a marked-up rate.

- Choose your casino account currency to match your funding source currency.

- Avoid letting the cashier auto-convert if you can pay in your account currency.

- If you use an e-wallet, keep a balance in the same currency you use at the casino.

Verify your account early

Late verification causes failed withdrawals. Failed withdrawals often mean extra processing time and sometimes extra charges by your provider. Get approved before you deposit large amounts or request a payout. Use a single clear set of documents and keep names and addresses consistent.

- Verify identity and address as soon as the casino allows it.

- Make sure your casino profile matches your documents, including middle names and abbreviations.

- Keep payment method ownership proof ready if the casino asks for it.

For step-by-step help, use this identity verification guide.

Batch withdrawals and plan timing

Many casinos cap free withdrawals by count, not by amount. If you withdraw small amounts often, you can hit a weekly or monthly limit and pay per withdrawal after that.

- Withdraw less often, in larger amounts, if your budget allows it.

- Check daily and weekly withdrawal limits before you play.

- Avoid canceling and re-submitting withdrawals unless support tells you to. Some casinos reset your queue position.

Meet bonus rules to avoid forfeits and capped cashouts

Bonus terms can create indirect costs. You can lose funds through forfeiture, reduced cashout limits, or forced conversion to less favorable withdrawal methods.

- Track wagering progress and deadline dates.

- Follow game contribution rules, especially for slots versus table games.

- Check max bet limits while wagering a bonus. A breach can void winnings.

- Confirm max cashout caps on bonus winnings before you accept the offer.

Watch inactivity rules and set reminders

Some casinos charge dormancy or inactivity fees after a set period with no logins or no transactions. These charges can drain a small balance.

- Read the inactivity window in the Terms and note the fee amount.

- Set a reminder before the dormancy period ends.

- Withdraw small leftover balances instead of leaving them idle.

Use fee waivers strategically

Casinos often waive fees through account tiers or scheduled promos. Use these to reduce predictable charges.

- VIP tiers, higher tiers may include more free withdrawals or faster processing.

- Promo days, some sites offer fee-free withdrawal windows or higher limits for a limited time.

- Withdrawal limits, if you face a low weekly cap, plan withdrawals around the cap to avoid extra requests.

- Ask support, when an intermediary bank deducts a fee, request reimbursement if the casino policy allows it.

Bonus and promo terms that can increase your effective costs

Wagering requirements change your real cost to cash out

A bonus can raise your effective costs even if the casino charges zero transaction fees. Wagering requirements force extra betting before you can withdraw. Those extra spins or hands create expected losses. Treat that expected loss as a fee you pay to access the bonus.

Check these fields before you claim any promo:

- Wagering multiple, like 30x, 40x, 60x.

- What counts toward wagering, deposit only, bonus only, or deposit plus bonus.

- Time limit, short deadlines push you into faster, higher-variance play and more errors.

- Restricted games, some games may not count at all.

Use a simple estimate to compare offers:

- Required wagering = (amount the casino requires) x (wagering multiple).

- Expected cost = required wagering x house edge of the games you will use.

Max cashout, max bet, and game contribution rules can block withdrawals

Many bonuses cap what you can withdraw. Others cap your bet size while you clear wagering. Both can turn a good session into a limited payout, or a voided bonus.

- Max cashout, the casino limits how much bonus-derived money you can withdraw, like 5x the bonus or a fixed amount. Any winnings above the cap get removed.

- Max bet, the casino sets a maximum stake per spin or per hand while a bonus is active, like $5. If you exceed it, the casino may void winnings or remove the bonus balance.

- Game contribution, some games count 100%, others 10% or 0% toward wagering. If you use low-contribution games, you need far more betting volume to qualify for a withdrawal.

- Excluded games, table games and live dealer often count 0% or trigger extra limits. Some sites also exclude certain slots.

Action step. Open the promo terms and search for, max cashout, max bet, contribution, excluded games, and restricted games. If you cannot follow those limits, skip the bonus.

Sticky vs. non-sticky bonuses change what you can withdraw

Bonus type controls how your money gets used and what you can take out.

- Non-sticky bonus, you play with your cash first. You can often withdraw your remaining deposit balance at any time, but you may lose the bonus if you do.

- Sticky bonus, you play with the bonus first. The casino may lock your deposit until you meet wagering. Some sites also remove the bonus when you withdraw, which can erase part of your balance if the bonus sits in the same wallet.

Practical impact. Sticky bonuses can act like a withdrawal fee, because you pay with extra wagering or you give up the bonus and its attached winnings to access your own funds.

Some deposit methods restrict your withdrawal options

Payment rules can create extra steps and extra charges.

- Method matching, casinos often require you to withdraw back to the same method you used to deposit, up to the deposit amount. If that method cannot accept payouts, you must switch methods.

- Alternative payout rails, switching can push you into bank transfer, checks, or other options where intermediary fees are more common.

- Extra processing time, method changes often add reviews and delays, which can matter if the bonus has a short validity window.

Before you deposit, confirm that your chosen method supports withdrawals in your country and currency. For step-by-step help, use our guide on how to withdraw money from an online casino.

Bonus abuse clauses can create fee-like outcomes

Many casinos include broad terms that let them reverse promo value when they detect behavior they classify as abuse. You may not pay a posted fee, but you can lose money in a similar way.

- Voided winnings, the casino cancels winnings tied to a bonus if it flags max bet breaches, restricted game use, or irregular patterns.

- Confiscated bonus, the casino removes the bonus and any bonus-linked winnings if you withdraw before clearing, use multiple accounts, or use mismatched payment methods.

- Delayed payouts, the casino may hold the withdrawal during investigations, which can also reset promo eligibility or trigger time limits.

Reduce the risk. Use one account, one set of payment methods in your name, and stay under the max bet. Keep screenshots of the promo terms you accepted, including caps and contribution rules.

Red flags and fairness checks: spotting expensive or predatory fee policies

Unusually high withdrawal percentages and unclear fee tables

Start with the withdrawal fee line. Many fair casinos charge a flat fee, or no fee, for standard methods. Predatory policies take a percentage.

- Percentage fees on withdrawals. Watch for 2% to 10% fees, or “up to” language with no examples. A 5% fee on a $1,000 cashout costs you $50.

- Fee tables that hide the real cost. Red flags include missing caps, missing minimums, or fees shown only inside a cashier screen after you deposit.

- Currency and conversion traps. If the casino forces account currency conversion, you can pay a spread plus a separate “FX fee.” Look for the rate source and the exact percentage.

- “Free” withdrawals with conditions. Some casinos waive fees only if you cash out above a high minimum, or only for one method. You still pay when you use anything else.

| Policy detail | What it can cost | Fairer alternative |

|---|---|---|

| 5% withdrawal fee | $50 per $1,000 | $0, or a small flat fee |

| “Fees may apply” with no table | Unknown until cashout | Full fee table in T&Cs |

| Mandatory conversion to casino currency | FX spread plus fee | Let you hold your local currency |

Frequent “failed withdrawal” loops and repeated processing deductions

Some casinos turn withdrawals into a loop. Each attempt creates a new “processing” event, and you pay each time.

- Repeated “failed withdrawal” outcomes. If the casino rejects a valid method with vague reasons, treat it as a cost risk. You can lose time and fees across multiple attempts.

- Processing fees charged per attempt. Check if the terms say fees apply “per transaction” or “per withdrawal request.” That wording matters.

- Method switching pressure. If support pushes you to a different method “to speed it up,” confirm the new method’s fees before you accept. Some alternatives carry higher charges or worse FX rates.

- Chargeback style penalties. Some terms add extra fees if you reverse a deposit, cancel a withdrawal, or trigger “manual review.” Look for fixed penalties and admin fees.

Log every attempt. Save timestamps, error messages, and the fee line from the cashier. If a withdrawal stays stuck, use a clear process, see our guide on why a withdrawal may show as pending.

Aggressive inactivity fees and short dormancy windows

Inactivity fees drain balances fast. The worst policies start early and charge monthly until your balance hits zero.

- Short dormancy windows. Red flags include 30 to 90 days with no “real money play” requirement defined. Some count only wagering, not logging in.

- High monthly deductions. Watch for $5 to $15 per month, or a percentage of your balance. A percentage fee scales up as your balance grows.

- Hard-to-stop fees. If the terms say you must contact support to stop fees, expect delays. A fair policy stops when you log in and verify activity.

- Fees that apply to bonuses and winnings. Some casinos treat bonus balances as eligible for inactivity deductions, which can wipe pending winnings tied to wagering rules.

Protect yourself. Withdraw idle balances. Keep one small deposit method active only if you plan to play. Do not leave money sitting for months.

Unlicensed or weakly regulated operators with vague banking terms

Weak regulation often means weak fee rules. You see vague banking terms, broad discretion, and few limits on charges.

- “We may charge fees at our discretion.” This line lets the casino change costs after you deposit.

- No defined payout timelines. If terms avoid clear timeframes for withdrawals, you risk long holds and extra verification steps.

- Undefined third-party costs. “Intermediary bank fees may apply” can be real, but fair casinos explain when it happens, for which methods, and who pays.

- Restrictions that force expensive methods. Some casinos block low-cost cashouts and push you into wire transfers or “manual payouts” with fees.

How to verify licensing, payment security, and complaint history

- Verify the license number. Find the license in the site footer and in the terms. Click through to the regulator site if possible. Match the operator name and domain.

- Check the regulator quality. Prefer well known gambling authorities with public license lookups and enforcement history. Avoid “licenses” you cannot verify.

- Read the banking and fee terms in full. Look for a clear fee table, clear caps, and clear “per transaction” language. Save a copy before you deposit.

- Confirm payment security. In the cashier, look for HTTPS, 3DS for card payments, and reputable PSP brands. Avoid sites that ask for card details over email or chat.

- Search complaint patterns. Focus on repeated reports of fee deductions, forced method changes, and endless verification holds. One-off complaints matter less than patterns.

- Test with a small amount. Make a small deposit, then a small withdrawal, before you commit. Measure speed, fees, and support clarity.

If the fee policy reads vague, changes often, or penalizes normal cashouts, treat it as a risk. Pick a casino with transparent costs and predictable withdrawal rules.

Compliance, responsible gambling, and why fees sometimes exist

KYC and AML checks can slow payouts

Casinos must follow KYC and AML rules. They need to know who you are, where you live, and that your funds come from a legal source. These checks can add time to your first withdrawal, and they often trigger when you change details or cash out a large amount.

- When delays happen: first withdrawal, new payment method, change of address, big win, unusual deposit patterns, chargeback history.

- What they may ask for: photo ID, proof of address, payment method proof, sometimes source of funds.

- How it affects fees: you can miss a free withdrawal window, hit an inactivity fee, or get pushed into a different method with higher charges if verification drags on.

- What to do: verify early, keep your account details consistent, and upload clear documents in one batch. Use this guide for steps and common rejection reasons: verify your identity faster.

Anti-fraud rules explain many withdrawal restrictions

Some fees exist because fraud and chargebacks cost money. Casinos try to control that risk with method rules. The strict versions feel like penalties, but the goal is to stop stolen cards, bonus abuse, and laundering.

- Same-method withdrawal rules: many casinos return funds to the original deposit method first. This reduces card fraud and disputes.

- Why prepaid and vouchers often cannot cash out: Paysafecard and similar products usually do not support withdrawals. Casinos route withdrawals to bank transfer or an e-wallet instead. That switch can add a fee.

- Why some cards fail on withdrawal: many cards support deposits but block gambling payouts. Your bank, card network, or issuer rules can force a different method.

- What to do: pick a method that supports both deposit and withdrawal before you fund your account. Avoid mixing methods unless you accept extra checks and possible charges.

Gambling blocks and issuer declines can create extra charges

Banks and card issuers often block gambling transactions. Some blocks stop deposits. Others allow deposits but reject refunds or payouts. Repeated declines can also trigger extra checks on the casino side.

- Common causes: gambling merchant blocks, country restrictions, MCC filtering, 3D Secure failures, daily spend limits, compliance flags.

- What to do first: call your bank and ask them to allow gambling transactions for the specific merchant type. Ask if they block both deposits and payouts.

- If your bank will not allow it: use a regulated e-wallet that supports gambling transactions, or use bank transfer where available.

- How this ties to fees: failed deposits can still trigger bank fees in some cases. Forced method changes can add casino withdrawal fees or third-party transfer fees.

Responsible gambling tools help you control spend beyond fees

Transaction charges matter, but your biggest cost usually comes from overspending. Use control tools that reduce harm before you need to worry about small payment fees.

- Deposit limits: set daily, weekly, or monthly caps. Do this before your first deposit.

- Loss limits and wager limits: cap what you can lose or stake in a time period.

- Session limits and reality checks: get timed prompts, then log out on schedule.

- Cooldown and self-exclusion: lock your account for days, months, or longer. Use this if limits do not hold.

- Bank-level controls: use a gambling block on your card if you keep breaking your rules.

Quick checklist: minimize fees before, during, and after you play

Before depositing: lock your basics

- Match your currency. Pick a casino wallet currency that matches your bank or e-wallet. Avoid forced FX on every deposit and withdrawal.

- Pick one primary payment method. Use the same method for deposits and withdrawals when possible. This reduces “closed loop” friction, extra checks, and forced method switches that can trigger extra fees.

- Check the fee table before you fund. Scan cashier terms for deposit fees, withdrawal fees, currency conversion rates, minimums, and maximums.

- Set limits before the first deposit. Use deposit limits, loss limits, wager limits, and session limits. You cut overspending and you cut fee exposure from extra transactions.

| Fee checkpoint | What to confirm | What you do |

|---|---|---|

| Deposit fee | Casino charges a % or fixed fee on deposits | Switch method, or deposit less often with larger amounts |

| Withdrawal fee | Free withdrawals per month, fixed fee after | Batch withdrawals, stay under the free allowance |

| FX markup | Rate used for conversion, extra “exchange” fee | Use matching currency, avoid DCC, use a multi-currency wallet |

| Minimum and maximums | Min deposit, min cashout, max per transaction | Plan amounts to avoid forced extra transactions |

| Method restrictions | Some methods allow deposit only, not withdrawal | Choose a method that supports both directions |

| Intermediary charges | Bank wire and international transfer deductions | Prefer local transfer options, or e-wallets where available |

During play: protect your bonus and your cashout

- Track your bonus status. Know the wagering requirement, expiry, max bet, and game contributions. A rule break can void winnings and turn “fees” into a total loss.

- Avoid restricted games. Some bonuses exclude live dealer, jackpots, or low contribution slots. Confirm before you spin.

- Do not do “cashout then re-deposit” loops. Some casinos treat this as bonus abuse and delay or reject withdrawals.

- Keep clean records. Save bonus emails, promo pages, and screenshots of key terms. Use them if support disputes a cashout.

Before withdrawing: remove delays, reduce transaction count

- Finish KYC early. Submit ID, proof of address, and payment proof before you request your first withdrawal. Use the casino’s exact file rules to avoid re-uploads. Read a clear breakdown in this online casino KYC guide.

- Use a batching strategy. If the casino charges per withdrawal, take fewer withdrawals. If it caps maximum cashout per transaction, plan a schedule that minimizes total payouts.

- Time it right. Request withdrawals during support hours and before weekend cutoffs. Expect longer processing when you trigger manual checks.

- Confirm method and currency. Withdraw to the same method you used to deposit, and in the same currency when possible. This reduces forced conversions and payment reroutes.

- Check pending status fast. If a withdrawal sits in “pending” too long, contact support with your transaction ID and timestamps.

After withdrawal: reconcile to catch hidden deductions

- Match amounts line by line. Compare requested amount, approved amount, and received amount. Log dates, currency, and reference numbers.

- Identify the deduction source. Separate casino fees from processor fees, bank fees, and FX. Ask your bank for the fee code if you see an unexpected shortfall.

- Check FX rate used. Compare the applied rate to a mid-market reference at the same time and date. Record the spread.

- Fix it for next time. If you see intermediary deductions, switch to a different rail, use a local transfer option, or withdraw to a multi-currency wallet.

- Keep a fee log. Track totals per month. You will see patterns fast and you can adjust deposit and withdrawal frequency.

FAQ

What fees can an online casino charge for payments?

Common charges include deposit fees, withdrawal fees, currency conversion markups, intermediary bank fees for wire transfers, and fees for inactive accounts. Some casinos also charge for extra withdrawals each month. Your payment provider can add its own fees on top.

Do casinos charge fees on deposits?

Some do, some do not. Card deposits may trigger merchant fees, cash advance fees, or foreign transaction fees from your bank. E-wallets can charge funding fees. Always check the cashier screen before you confirm.

Do casinos charge fees on withdrawals?

Many casinos offer free withdrawals, then charge after a set number per month, or above a threshold. Bank transfers often cost more due to fixed fees. Card withdrawals can fail and force a different method, which can add extra charges.

What are intermediary bank fees and who pays them?

Intermediary banks can deduct fees during international wire transfers. You usually pay them through a smaller net payout. The casino may also charge a sending fee. Use local transfer options or e-wallet withdrawals to avoid most intermediary deductions.

How can you spot a hidden FX fee?

Compare the rate used on your receipt to a mid-market rate at the same time. The gap is your spread. Card processors and e-wallets often add 1% to 4%. Multi-currency wallets help if you can hold and withdraw in the casino currency.

Why do casinos push you to withdraw to the same method you used to deposit?

AML rules and card scheme rules drive this. Casinos must return funds to the source when possible. If you switch methods, you may trigger extra checks or forced routing, which can add fees and delay your payout.

Can bonuses increase your transaction costs?

Yes. Wagering rules can push you to keep funds longer, then withdraw later in smaller chunks. Some casinos also limit withdrawal amounts per day or week for bonus play. That can mean more withdrawals and more fees.

What is the cheapest way to move money in and out?

It depends on your country and casino currency. In general, local bank transfer rails and major e-wallets tend to cost less than international wires. Avoid unnecessary currency conversion. Keep deposits and withdrawals in the same currency when you can.

What should you do if your withdrawal arrives short?

Save screenshots of the withdrawal request and the cashier receipt. Ask the casino for a transfer reference and fee breakdown. Then ask your bank or provider about incoming deductions. If the casino refuses to explain, use the complaint and ADR process.

Do KYC checks affect fees?

They can. Delays can force you to retry withdrawals, hit monthly limits, or use a different method. That can add provider fees and FX costs. Verify early, keep documents current, and match your payment account name to your casino profile.

How do you reduce fees fast?

- Use one method for both deposits and withdrawals.

- Withdraw less often, in larger amounts, if your casino charges per withdrawal.

- Avoid FX by using the casino account currency.

- Track each fee in a monthly log and change rails when patterns appear.

Conclusion

Conclusion

Casino fees rarely show up as one big charge. They leak out through deposit fees, withdrawal fees, FX spreads, bank lifting fees, and processor markups. If you do not track them, you will keep paying them.

Your final move is simple. Build a repeatable payment setup and stick to it. One method in, the same method out. One account currency, no conversion. Fewer withdrawals, larger amounts. A quick log that shows what each cashout really cost.

- Pick your main rail based on total cost, not brand. Include FX and bank fees in the number.

- Lock your currency to the casino account currency and your wallet or bank currency.

- Standardize your cashouts with a set threshold so you avoid per-withdrawal charges.

- Review monthly and switch only when the data shows a cheaper route.

If speed drives your choice, pair your fee log with a clear view of processing delays. Use this guide on online casino payout times to avoid methods that cost you in both fees and waiting.

-

Online Casino KYC Explained: Verification Process, ID Checks, Age Rules & AML

4 months ago -

How to Sign Up & Create an Online Casino Account (Step-by-Step)

4 months ago -

How to Verify Your Identity at an Online Casino (and Get Approved Faster)

4 months ago -

How to Withdraw Money from an Online Casino: Methods, Steps & Tips

4 months ago -

Online Casino Payout Times Explained: How Long Withdrawals Take (and Why)

4 months ago

-

- Deposit fees, when “free deposits” is not truly free

- Withdrawal fees, flat fees, percentage fees, and tiered schedules

- Currency conversion (FX) charges and dynamic currency conversion pitfalls

- Bank and card issuer fees, cash advance, gambling blocks, and international charges

- E-wallet and prepaid voucher charges, loading, transfer, and withdrawal costs

- Inactivity, dormancy, and account maintenance fees

- Chargeback and dispute-related fees (and when they apply)

- Bonus-related costs, wagering requirements, max cashout rules, and forfeiture triggers

-

- Payment methods compared: likely charges, speed, and best use cases

- Credit and debit cards (Visa, Mastercard): when card deposits become expensive

- Bank transfer and instant banking: fee risks and processing timelines

- E-wallets (PayPal, Skrill, Neteller): convenience vs. provider-side charges

- Prepaid cards and vouchers (PaysafeCard): where fees and limits typically bite

- Crypto payments: network fees, spreads, and volatility considerations

- Mobile payment options: carrier rules, limits, and potential surcharges

-

- Unusually high withdrawal percentages and unclear fee tables

- Frequent “failed withdrawal” loops and repeated processing deductions

- Aggressive inactivity fees and short dormancy windows

- Unlicensed or weakly regulated operators with vague banking terms

- How to verify licensing, payment security, and complaint history

-

- What fees can an online casino charge for payments?

- Do casinos charge fees on deposits?

- Do casinos charge fees on withdrawals?

- What are intermediary bank fees and who pays them?

- How can you spot a hidden FX fee?

- Why do casinos push you to withdraw to the same method you used to deposit?

- Can bonuses increase your transaction costs?

- What is the cheapest way to move money in and out?

- What should you do if your withdrawal arrives short?

- Do KYC checks affect fees?

- How do you reduce fees fast?

-

- Deposit fees, when “free deposits” is not truly free

- Withdrawal fees, flat fees, percentage fees, and tiered schedules

- Currency conversion (FX) charges and dynamic currency conversion pitfalls

- Bank and card issuer fees, cash advance, gambling blocks, and international charges

- E-wallet and prepaid voucher charges, loading, transfer, and withdrawal costs

- Inactivity, dormancy, and account maintenance fees

- Chargeback and dispute-related fees (and when they apply)

- Bonus-related costs, wagering requirements, max cashout rules, and forfeiture triggers

-

- Payment methods compared: likely charges, speed, and best use cases

- Credit and debit cards (Visa, Mastercard): when card deposits become expensive

- Bank transfer and instant banking: fee risks and processing timelines

- E-wallets (PayPal, Skrill, Neteller): convenience vs. provider-side charges

- Prepaid cards and vouchers (PaysafeCard): where fees and limits typically bite

- Crypto payments: network fees, spreads, and volatility considerations

- Mobile payment options: carrier rules, limits, and potential surcharges

-

- Unusually high withdrawal percentages and unclear fee tables

- Frequent “failed withdrawal” loops and repeated processing deductions

- Aggressive inactivity fees and short dormancy windows

- Unlicensed or weakly regulated operators with vague banking terms

- How to verify licensing, payment security, and complaint history

-

- What fees can an online casino charge for payments?

- Do casinos charge fees on deposits?

- Do casinos charge fees on withdrawals?

- What are intermediary bank fees and who pays them?

- How can you spot a hidden FX fee?

- Why do casinos push you to withdraw to the same method you used to deposit?

- Can bonuses increase your transaction costs?

- What is the cheapest way to move money in and out?

- What should you do if your withdrawal arrives short?

- Do KYC checks affect fees?

- How do you reduce fees fast?

-

Reload Bonus Explained: What It Is and When It’s Worth Claiming

1 month ago -

Online Casino Licensing Explained: Authorities, Licenses & How to Check One

3 months ago -

Best Live Dealer Casinos: Where to Play Live Blackjack, Roulette & More

3 months ago -

Best Online Casinos for High Rollers: VIP Perks, High Limits & Exclusive Bonuses

3 months ago -

Fast Payout Online Casinos: Best Sites for Quick Withdrawals

3 months ago

-

Online Casino Licensing Explained: Authorities, Licenses & How to Check One

3 months ago -

Are Online Casinos Legal? Complete Guide by State & Country

4 months ago -

Casino VIP & Loyalty Programs Explained: Points, Tiers, Rewards & Rakeback

4 months ago -

Online Casino Fairness Explained: RNG, RTP, House Edge & Provably Fair

4 months ago -

Free Spins Bonus Explained: How Free Spins Work at Online Casinos

4 months ago