Online Casino Payment Methods Compared: Fees, Speed, Limits & Best Options

Payment choice affects your money. It sets your costs, your withdrawal speed, and how much you can move in one go.

This guide compares the main online casino payment methods, cards, bank transfers, e-wallets, prepaid vouchers, and crypto. You will see typical deposit and withdrawal times, common fees, and usual minimums and maximums. You will also learn where players get stuck, slow cashouts, failed withdrawals, and limit caps.

Use this to pick the best option for your deposit and your cashout, based on speed, cost, and approval rate. For the fee breakdown and the extra charges casinos and payment providers add, see online casino fees and transaction charges.

- In het kort: Pick one method for deposits and one for cashouts, they do not need to match.

- In het kort: Bank transfer gives higher limits, it often pays slower.

- In het kort: Cards deposit fast, withdrawals often route to bank and can take longer, some casinos do not allow card cashouts.

- In het kort: E-wallets often cash out faster and with fewer failures, but fees and limits depend on your wallet tier and country.

- In het kort: Crypto can pay fast, approval depends on correct wallet address, network, and casino rules, fees vary by chain.

- In het kort: Prepaid vouchers work for deposits, many do not support withdrawals, plan your cashout method first.

- In het kort: Most payout delays come from verification, mismatched names, or method restrictions, not from the casino cashier screen.

Key takeaways

- Speed: E-wallets and crypto usually deliver the fastest withdrawals. Bank transfers usually take longer. Cards sit in the middle, and can be slow if the casino routes payouts to your bank.

- Fees: You pay fees in three places, the casino, the payment provider, and the network. FX conversion is a common hidden cost. Use the same currency end to end when you can.

- Limits: Banks and crypto often support higher maximums. Cards and wallets can cap you per transaction, per day, or by account tier.

- Approval rate: You get fewer failed withdrawals when your name matches your casino profile, you use a supported payout method, and you avoid chargeback linked methods for cashouts.

- Common failure points: Wrong bank details, wrong crypto network, expired cards, wallet account not verified, or the casino blocks withdrawals to deposit only methods.

- Best default setup: Use cards or instant bank for deposits, then use e-wallet, bank transfer, or crypto for withdrawals, based on your limits and speed needs.

- Reduce delays: Complete checks early, upload clear documents, and keep your payment account and casino account details identical. Read how to verify your identity at an online casino.

What “Online Casino Payment Methods Comparison” Should Include (Fees, Speed, Limits, Safety)

Deposit vs withdrawal, why they differ

Deposits usually clear fast. The casino gets funds and can credit your balance at once.

Withdrawals take longer. The casino must run checks, approve the payout, and push money out through the provider.

- More checks on withdrawals: KYC, fraud screening, and responsible gambling controls can delay approval.

- Method mismatch causes failures: Some casinos require you to withdraw to the same method you used to deposit, or they cap card withdrawals and route the rest by bank transfer.

- Name and details must match: Your casino profile, bank account, and wallet account should use identical personal details.

Typical fee types to compare

- Casino fees: Some casinos charge a withdrawal fee, a fee after a set number of free withdrawals, or a fee for small payouts.

- Provider fees: E-wallets, card networks, and payment apps may charge cash-out or transfer fees.

- Bank fees: Your bank can charge incoming wire fees, intermediary bank fees, or rejection and return fees for wrong details.

- FX spreads: If your deposit currency differs from the casino wallet currency, or your withdrawal hits a different currency account, you pay the spread and sometimes a conversion fee.

- Blockchain network fees: Crypto payouts include network fees. They change with congestion. The casino may also add a crypto handling fee.

Key speed metrics to track

- Instant deposit time: How fast your balance updates after you authorize the payment.

- Pending time: How long the transaction sits as pending before the casino or provider marks it complete.

- Casino processing time: How long the casino takes to approve a withdrawal before it sends it out.

- Settlement time: How long the provider, bank, or blockchain takes to deliver funds after approval.

Compare methods using total payout time, casino processing time plus settlement time. A fast method still feels slow if the casino holds payouts for review.

Limits explained, what numbers matter

- Minimums: The smallest deposit or withdrawal allowed. Some methods block small cash-outs.

- Maximums: The biggest amount per transaction. Large withdrawals often require splitting.

- Rolling limits: Caps per day, week, or month. You can hit these even if each transaction stays under the max.

- Method-specific caps: Cards often have lower withdrawal caps. Bank transfer and crypto often support larger payouts. Some wallets limit based on account tier and verification level.

Safety basics to include in a comparison

- Encryption: Look for HTTPS and modern TLS to protect data in transit.

- 3D Secure for cards: Adds a bank approval step. It cuts fraud and reduces chargeback risk, but can cause failures if your bank blocks gaming transactions.

- Tokenization: The casino stores a token, not your full card number. It lowers exposure in a breach.

- Account protection: Use strong passwords, unique emails, and 2FA where available. Lock your payment account with alerts for logins and transfers.

Quick comparison table, what to check for every method

| Category | What to record | Why it matters |

|---|---|---|

| Fees | Casino fee, provider fee, bank fee, FX spread, network fee | Shows true cost, prevents surprises on cash-out |

| Speed | Deposit time, casino processing time, settlement time | Predicts real payout timing |

| Limits | Min, max, rolling caps, per-method withdrawal caps | Determines whether you can move your normal stakes and wins |

| Success rate | Common declines, required matching deposit method, KYC triggers | Reduces rejected or reversed payments |

| Safety | 3D Secure, tokenization, 2FA options, fraud controls | Lowers fraud risk and account takeover risk |

If you want fewer payout delays, complete KYC early and keep your details consistent. Use casino identity verification before you request your first large withdrawal.

At-a-Glance Comparison Table (Quick Decision Guide)

Use this table to pick a method fast. Match it to your goal, your bank country, and your casino’s rules.

| Method | Deposit speed | Withdrawal speed | Typical fees | Limits | Best for | Key watchouts |

|---|---|---|---|---|---|---|

| E-wallets (Skrill, Neteller, PayPal) | Instant | Minutes to 24 hours | Usually low, FX can be high | Medium to high | Fast cashouts, mobile | Wallet KYC, possible withdrawal fee, FX spread |

| Pay-by-bank (instant bank transfer, open banking) | Instant to minutes | Same day to 1 business day | Often low, bank fees vary | Medium to high | Low friction deposits, solid limits | Name must match, bank may block gambling, return risk if details mismatch |

| Cards (Visa, Mastercard) | Instant | 1 to 5 business days | Often none, cash advance and FX possible | Low to medium | Easy deposits | Many card cashouts fail, 3D Secure declines, withdrawal may go to bank transfer instead |

| Bank transfer (SEPA, local, wire) | Same day to 3 business days | 1 to 5 business days | Low to medium, wires can cost more | High | Big withdrawals, VIP | Strict KYC, wrong details cause returns, slower processing |

| Prepaid vouchers (PaysafeCard) | Instant | Often not supported | Voucher fees possible | Low | Privacy for deposits | You still need a cashout method, limits stay low |

| Crypto (BTC, ETH, USDT) | Minutes to hours | Minutes to 24 hours | Network fees, exchange fees | Medium to very high | Speed, high limits, borderless | Volatility, wallet mistakes are final, casino may require source of funds proof |

| Mobile wallets (Apple Pay, Google Pay) | Instant | Rare, usually not direct | Usually none, card FX possible | Low to medium | Fast mobile deposits | Often deposit only, cashout goes to card or bank |

Best for fast withdrawals

- E-wallets. Expect minutes to 24 hours after approval. Best when your wallet name matches your casino profile.

- Crypto. Expect minutes to a few hours after approval, plus blockchain time. Use stablecoins if you want less price risk.

- Pay-by-bank. Expect same day to 1 business day. Works well when your bank supports instant rails.

Best for low total cost

- Pay-by-bank. You often avoid card cash advance fees and wallet FX markups. Check if your bank charges transfer fees.

- Local bank transfer. Best for same currency play. You reduce FX losses if your casino balance matches your bank currency.

- Cards. Low visible fees, but watch hidden costs. Avoid deposits that code as cash advance, avoid dynamic currency conversion.

Best for high limits

- Bank transfer and wire. Best for large withdrawals. Expect extra checks and longer approval time.

- Crypto. High ceiling if the casino supports it. You may still face internal per transaction caps.

- Verified e-wallets. Higher limits after wallet KYC. Some casinos tier limits by VIP level.

Best for privacy

- Prepaid vouchers. Private for deposits only. You still need a verified method to withdraw.

- Crypto. Pseudonymous, not anonymous. Casinos often link your wallet to your verified account and can ask for source of funds.

- Cards and bank. Lowest privacy. Your bank statement shows the merchant or processor name.

Best for mobile

- E-wallet apps. Fast login, one tap confirmations, easy balance control. Keep 2FA on.

- Apple Pay and Google Pay. Best deposit flow. Expect withdrawals to route to card or bank.

- Pay-by-bank. Strong mobile flow with bank app approval. Fewer failed deposits than manual bank transfers.

If your withdrawal fails or reverses, check method matching rules, name mismatches, and pending KYC first. Use this guide on why your casino withdrawal was rejected.

E-Wallets (Skrill, Neteller, PayPal & More)

E-Wallets (Skrill, Neteller, PayPal & More)

E-wallets sit between your casino and your bank. You fund the wallet once, then deposit fast across sites. You withdraw to the wallet, then move money to your bank when you choose.

Where e-wallets win

- Faster withdrawals. Many casinos process e-wallet cashouts quicker than bank transfers. You often see funds the same day after approval.

- One login for many casinos. You avoid typing card details every time. You also reduce failed deposits caused by card issuer blocks.

- Separation from your bank account. The casino never sees your bank details. You keep cleaner spend tracking and tighter bankroll control.

- Good for mobile. Most wallets support app logins, biometrics, and simple confirmations.

Common drawbacks

- Wallet-to-bank fees. Some wallets charge for withdrawals to your bank, currency conversion, or receiving international transfers. Check the fee table inside your wallet before you cash out.

- Verification holds. Wallets and casinos both run checks. First-time payouts can stall until you confirm identity and address. Use this guide on how to verify your identity faster.

- Merchant restrictions. PayPal works well in some markets and fails in others. Some casinos accept PayPal for deposits but limit withdrawals to bank. Skrill and Neteller support gambling more widely, but rules still vary by country and operator.

- Method matching rules still apply. If you deposit with a wallet, the casino often requires you to withdraw back to the same wallet up to your deposit total.

Typical limits and funding sources

Your real limits come from three places, your wallet status, your casino limits, and your funding source.

| Funding route | Deposit speed | Typical friction | What it means for casino payouts |

|---|---|---|---|

| Card to wallet | Instant | Card issuer blocks, higher fees, 3DS checks | You can deposit instantly, but you may need extra wallet verification before larger withdrawals clear. |

| Bank to wallet | Fast to 1 business day | Bank transfer steps, occasional bank approval | Usually smoother for higher volumes and fewer card-related declines. |

| Balance already in wallet | Instant | Low | Best flow for repeat play and quick re-deposits. |

- Minimum deposits often start low, but the casino sets the floor.

- Maximum deposits and withdrawals rise after KYC and after your wallet account reaches higher verification tiers.

- Currency conversion can be the hidden cost. Keep your casino and wallet in the same currency when possible.

When casinos restrict wallet withdrawals (and how to avoid it)

- You used a different method to deposit. Many casinos send withdrawals back to the original method first. Fix it by using the same wallet for deposits if you want wallet payouts.

- You deposited by card into the casino. Some operators force withdrawals to card or bank first, then allow wallet for excess winnings. Avoid mixed-method deposits if you care about payout speed.

- Bonus terms restrict withdrawal routes. Some bonuses block certain methods. Check the cashier notes before you opt in.

- Wallet not available in your region. The cashier may show it for deposits but block it for withdrawals due to local rules. Test with a small deposit before you commit.

- Name or email mismatch. Your casino and wallet must match. Use the same legal name and the same core contact details.

Best-fit player profiles

- Frequent cashouts. You want fast, repeat withdrawals and fewer bank delays.

- Multi-casino play. You move funds between sites without re-entering card details each time.

- Mobile-first users. You want app-based approvals and quick deposits on the go.

- Privacy-focused bankroll management. You prefer not to share bank details with every operator.

Card Payments (Visa, Mastercard, AmEx): Fast Deposits, Variable Withdrawal Experience

Card Payments (Visa, Mastercard, AmEx): Fast Deposits, Variable Withdrawal Experience

Cards work best for deposits. You get near instant funding in most cases. Withdrawals vary by casino, country, and issuer. Plan for a backup cashout method.

Why card deposits get declined: issuer blocks, MCC codes, and fraud rules

- Issuer gambling blocks. Many banks block gambling by default. Some let you enable it in your banking app. Others decline every attempt.

- MCC code rejection. Card networks tag merchants with a Merchant Category Code. If your issuer blocks that MCC, the casino deposit fails even if your card works elsewhere.

- Fraud and velocity rules. Multiple tries, new merchant activity, high amounts, or late-night deposits can trigger automated declines.

- Mismatch data. Your name, address, or country on file does not match the casino account. Some processors require an exact match.

- Cross border restrictions. If the casino processes through another country, your bank may decline it as a risk flag.

Fees to watch: cash-advance treatment, international charges, and FX conversion

- Cash-advance coding. Some issuers treat gambling deposits as a cash advance. You can pay a flat fee, a percent fee, and immediate interest with no grace period.

- International transaction fees. If the acquiring bank sits abroad, your issuer may add 1% to 3% even when the casino shows your local currency.

- FX conversion spread. If you deposit in a different currency, you pay the network rate plus issuer markup. Avoid double conversion by matching casino account currency to your card currency.

- Prepaid card limits. Some prepaid cards allow deposits but block gambling MCCs, or cap daily spend at low levels.

| Fee type | What triggers it | What you can do |

|---|---|---|

| Cash-advance fee and interest | Issuer codes deposit as cash advance | Use a debit card, use an e-wallet, or call your bank to confirm treatment |

| International fee | Merchant acquirer is overseas | Use a card with 0% foreign transaction fees, or switch method |

| FX conversion cost | Deposit currency differs from card currency | Set one base currency and stick to it |

Withdrawal realities: push-to-card availability and alternative cashout routes

- Push-to-card depends on the processor. Some casinos can send withdrawals back to Visa or Mastercard. Many cannot. AmEx support is often narrower.

- Debit works more often than credit. Credit cards may accept refunds only, not payouts beyond your deposit amount.

- Refund-first rules. Many casinos return withdrawals to the original deposit method up to the amount you deposited. The rest goes to another method.

- Fallback routes matter. If push-to-card is not available, casinos route withdrawals to bank transfer, e-wallets, or checks depending on region.

Before you deposit, check the cashier for the exact withdrawal options tied to your card. If the casino cannot pay out to card, deposit with the method you want to withdraw to.

3D Secure and chargebacks: what they mean for player safety and disputes

- 3D Secure adds a bank approval step. You confirm in-app, by SMS, or by biometric approval. It reduces fraud declines and protects you if someone uses your card.

- 3D Secure can increase approval rates. Issuers trust authenticated transactions more than non-authenticated ones.

- Chargebacks exist, but casinos fight them. If you file a dispute after gambling, the merchant can respond with logs, IP data, and 3D Secure proof. If you took bonuses, the terms also matter.

- Chargebacks do not replace support. Use the casino’s withdrawal process first. Chargebacks can lead to account closure and voided balances.

Best practices: reducing declines and improving approval rates

- Use a card that allows gambling. If your bank blocks it, switch banks or use an e-wallet.

- Match your account details. Use your real name and address. Keep them consistent across your bank and casino profile.

- Start small. Make a low first deposit to establish trust with issuer fraud systems, then increase.

- Avoid rapid retries. If you get a decline, wait. Repeated attempts can lock the card for online transactions.

- Enable 3D Secure. Turn on app approvals and notifications to confirm deposits fast.

- Keep one currency. Reduce FX costs by using the same currency for card, casino wallet, and withdrawals.

- Verify early. Casinos often hold withdrawals until you pass KYC. Use identity verification before your first cashout.

- Keep a withdrawal method ready. Add a bank account or e-wallet before you win. Do not wait until the withdrawal page blocks your card payout.

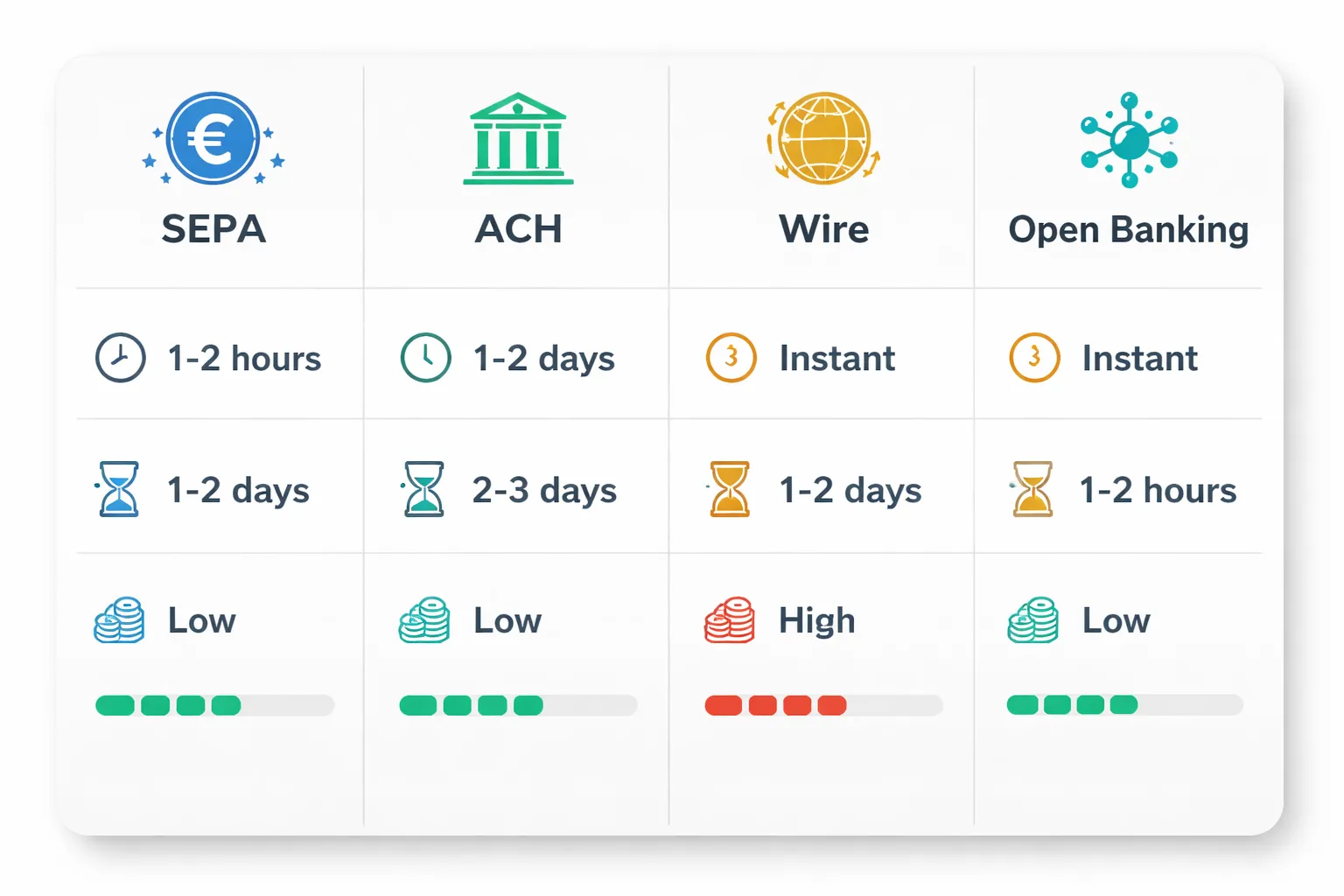

Bank Transfers & “Pay by Bank” (SEPA, ACH, Wire, Open Banking)

Bank transfers and “pay by bank” basics

Bank transfers move money from your bank account to the casino, or back to your bank. You will see three main rails, plus “pay by bank” via open banking.

- SEPA Credit Transfer, for EUR payments inside SEPA countries.

- ACH, for USD bank payments inside the United States.

- Wire, for domestic and international bank transfers, often used for high values.

- Pay by bank (open banking), you approve the transfer in your banking app. The casino gets instant account verification.

ACH vs SEPA vs wire, speed and cost expectations

| Method | Typical deposit speed | Typical withdrawal speed | Typical fees | Best for |

|---|---|---|---|---|

| SEPA | Same day to 1 business day | 1 to 3 business days | Often free or low fee at your bank, casino usually does not add a fee | EU players who want low cost EUR transfers |

| ACH | Same day to 2 business days | 2 to 5 business days | Usually low or none, some banks charge small fees for outgoing transfers | US players who want bank based payouts |

| Wire | Same day to 2 business days | 1 to 5 business days | Commonly high, bank fees and intermediary fees may apply | High limits, international transfers, when other rails fail |

| Pay by bank (open banking) | Minutes to same day, depends on local instant rails | Less common for withdrawals, where supported it can be faster than classic bank transfer | Usually no player fee, your bank may charge nothing | Fast deposits with instant account verification |

Expect bank processing windows. Weekends and bank holidays slow everything down. Wires can arrive fast, but cost more and trigger more checks.

Open banking flows, faster verification and fewer failures

Pay by bank works through your bank login or app approval. You confirm the payment. The provider returns proof that the account exists and matches you.

- Instant account verification. You reduce failed deposits from wrong account details.

- Cleaner audit trail. The casino sees a named bank account, which can help later withdrawals.

- Fewer chargeback issues. Bank transfers do not work like card chargebacks.

Availability depends on your country and bank. Some casinos use it for deposits only. Some support payouts to the same bank account after KYC.

Withdrawals, reliability versus longer processing windows

Bank withdrawals rarely fail if your details match. They also move slower than e-wallets.

- Reliable. You receive funds to your bank account, not to a third party wallet.

- Slower. Casinos often queue bank withdrawals for manual review. Banks then take extra business days.

- Harder to reverse. If you send funds to the wrong beneficiary, fixes take time.

If your casino restricts withdrawals to the original deposit method, a bank deposit can lock you into bank payouts. Plan for that before you choose it.

High limit transfers and extra checks

Higher limits bring stricter controls. Expect questions when you deposit or withdraw large sums by bank.

- Source of funds requests. Payslips, bank statements, or proof of sale may be required.

- Enhanced verification. More ID checks, proof of address, and sometimes a selfie check.

- Name matching. The casino will reject third party accounts. Your bank account name must match your casino profile.

Read the KYC requirements early. Use one verified bank account and keep it consistent. This reduces payout holds. For details, see casino KYC rules and AML checks.

How to avoid bank transfer delays

- Enter beneficiary details exactly. Use the correct IBAN for SEPA, routing and account number for ACH, and SWIFT plus IBAN or account number for wires.

- Use the required reference code. Many casinos issue a unique reference for matching your payment. Missing it causes manual review.

- Keep your name and address consistent. Match your bank profile to your casino profile.

- Do not split transfers unless asked. Multiple small transfers can trigger extra fraud checks.

- Send from your own account only. Third party transfers often get rejected and refunded.

- Time it. Submit withdrawals early in the day on a business day to avoid weekend dead time.

Prepaid & Voucher Methods (Paysafecard and Similar)

How vouchers work for deposits, and why withdrawals use a different method

Prepaid vouchers like Paysafecard work as pay-first deposit codes. You buy a voucher, then enter the PIN at checkout. The casino gets paid. No bank card details go to the casino.

Most casinos do not pay withdrawals back to a voucher. A voucher has no name and no receiving account. You usually withdraw to a bank transfer, card, or e-wallet instead. Some brands support Paysafecard accounts, but many still route withdrawals to another method to meet anti-fraud rules.

- Deposits: Enter voucher PIN, funds credit fast.

- Withdrawals: Pick a separate cash-out method, expect extra checks if your withdrawal method differs from your deposit method.

Fees and limits, activation, redemption, and caps

Your total cost depends on where you buy the voucher and whether you use a linked account. The casino usually charges no deposit fee for vouchers, but you can still pay fees at purchase or on account usage.

| Item | What you will see in practice |

|---|---|

| Voucher purchase fee | Often built into the retail price or added at checkout by the seller, varies by country and store. |

| Deposit fee at casino | Commonly 0%, but always check the cashier screen before confirming. |

| Voucher denominations | Fixed amounts, you may need multiple vouchers for one deposit. |

| Per deposit limit | Often capped, casinos may limit how many voucher PINs you can combine in one payment. |

| Account-level caps | Paysafecard and similar products can apply rolling limits, higher limits usually require account verification. |

Plan your cash-out path before you deposit. If your casino enforces method matching, you may need to verify an e-wallet or bank account before it approves a payout. For more on caps, see online casino withdrawal limits explained.

Privacy and control, tighter budgeting with less bank exposure

Vouchers keep your bank and card statements cleaner. You do not hand your card number to the casino. You also reduce chargeback disputes because the payment runs like cash. That can help if your bank blocks gambling merchant codes.

They also force discipline. You can only spend what you load. You can set hard limits by buying smaller denominations and stopping there.

- Less card exposure: No card details stored at the casino.

- Cleaner budgeting: You cap spend at the voucher value.

- Fewer bank declines: You avoid card issuer gambling blocks on deposits.

Common friction points: availability, region rules, and KYC triggers

Voucher payments look simple, but the friction usually hits at scale and at cash-out.

- Voucher availability: Stock varies by store. Some regions push you to online resellers, which can add fees or fraud risk.

- Region restrictions: Some casinos accept vouchers only in specific countries. Some vouchers work only in the country of purchase.

- Multi-voucher deposits: Large deposits may require many PINs, casinos may block too many codes in one transaction.

- KYC triggers: Big deposits, repeated deposits, or first withdrawal can trigger ID and address checks. Expect this even if vouchers feel anonymous.

- Withdrawal mismatch: If you deposit with vouchers and withdraw to a new method, the casino can ask for extra proof of ownership and source of funds.

Best use cases: deposit-only play and bankroll management

Use vouchers when you want fast deposits, tight control, and less bank exposure. Treat them as a deposit tool, not a full deposit and withdrawal solution.

- Deposit-only play: You want to fund an account quickly without using a card.

- Bankroll control: You want a hard ceiling per session, per week, or per trip.

- Backup method: Your bank blocks gambling deposits and you need a reliable fallback.

Mobile Payments (Apple Pay, Google Pay, Carrier Billing, Cash App Where Available)

One-tap deposits, faster checkout

Mobile payments such as Apple Pay, Google Pay, carrier billing, and Cash App where available focus on speed. You add funds with Face ID, Touch ID, or your device PIN. You skip typing card numbers at checkout.

In most casinos, Apple Pay and Google Pay use a tokenized version of your card. The casino never sees your full card number. The payment processor routes the charge to your underlying card or bank rail.

Availability caveats, support varies by casino

- Casino support: One casino may accept Apple Pay for deposits but block it for withdrawals. Another may not support it at all.

- Location rules: Legal status and payment rules change by country, and by state in the US. A method that works in one state can fail in another.

- Device setup: You need a compatible device, a funded wallet, and a verified card or bank source inside the wallet.

- Cash App: Some casinos accept Cash App via Cash App Pay, others treat it like a linked card. Support is market-specific and operator-specific.

- Carrier billing: Often limited to small deposits, and not offered at many regulated casinos.

Fees and limits, when mobile pay is just a card wrapper

Many “mobile pay” deposits price like card deposits because they are card deposits under the hood. Your casino may show it as Apple Pay or Google Pay, but the cost structure can still follow card rules.

| Method | Typical fee pattern | Typical limits pattern |

|---|---|---|

| Apple Pay, Google Pay | Often $0 from the casino, but can match card fee rules. Issuer may treat it as gambling or cash-like. | Often similar to card limits, plus wallet and bank issuer limits. |

| Cash App (where supported) | Can be $0 or handled like a card transaction, depends on the casino and routing. | Can be tighter than bank transfers, depends on verification level and operator limits. |

| Carrier billing | Often higher effective cost, or priced into exchange rates and service charges. | Usually low caps per transaction, per day, or per month. |

If your deposit fails, check your wallet funding source. Banks often block gambling MCCs. Switching the underlying card inside Apple Pay or Google Pay can fix it. If the casino shows “pending” after approval, see why your withdrawal is pending for common processing holds that also affect wallet-linked payments.

Withdrawal compatibility, deposits do not guarantee cash outs

Mobile payments often work as deposit rails first. Cashing out to the same method depends on the casino, the processor, and your region.

- Apple Pay, Google Pay: Many casinos cannot “send money to your wallet.” They may require a bank transfer, ACH, card refund flow, or an e-wallet for withdrawals.

- Cash App: Withdrawal support varies. Some casinos pay out to a linked bank account instead of Cash App directly.

- Carrier billing: Usually deposit-only. Do not plan on withdrawing this way.

Plan your exit before you deposit. If a casino does not support withdrawal to the same rail, use a method you can withdraw with, like bank transfer or a supported e-wallet.

Security advantages, less card exposure

- Tokenization: The casino receives a token, not your full card number.

- Device authentication: Face ID, Touch ID, and device PIN reduce the risk of stolen card details getting used online.

- Less data entry: You share fewer details at checkout, which cuts exposure on compromised devices and networks.

- Fast revocation: You can remove a card from your wallet, lock your phone, or disable the wallet quickly if needed.

Cryptocurrency Payments (BTC, ETH, USDT, and Altcoins)

Cryptocurrency Payments (BTC, ETH, USDT, and Altcoins)

Crypto deposits can clear fast. Crypto withdrawals can take longer. Speed depends on the chain, network load, and the casino’s approval step.

Transaction lifecycle: confirmations, mempool congestion, and real-world timing

- You send a deposit. Your wallet broadcasts a transaction to the network.

- It hits the mempool. If traffic spikes, your transaction waits until miners or validators pick it up.

- It gets confirmed. Casinos credit you after a set number of confirmations, not when you click send.

- Real timing varies. A “10 minute” chain can still take longer during congestion if your fee is low.

- BTC: Often reliable, but mempool backlogs happen. Low fees can mean long waits.

- ETH: Confirmation speed stays steady, but gas spikes can price you out at busy times.

- USDT: Speed depends on the network you choose. USDT on Tron often moves fast with low fees, USDT on Ethereum can cost more.

- Altcoins: Some are quick and cheap, some have thin liquidity and higher exchange costs.

True cost comparison: exchange spreads, wallet fees, and network gas fees

Crypto costs do not stop at “no deposit fee.” You pay through pricing and network fees.

- Exchange spread: You often lose value when you buy crypto. Thin markets and instant buy tools usually cost more.

- Exchange withdrawal fee: Many exchanges charge a fixed fee to send coins to a casino address.

- Network fee: BTC uses miner fees. ETH uses gas. Token transfers add their own gas needs. Fees rise when networks get busy.

- Casino conversion rate: If the casino converts your crypto to fiat on receipt, the rate can include a margin.

| Cost item | Where you see it | What to watch |

|---|---|---|

| Spread | Buying or swapping crypto | Instant purchase rates, low liquidity pairs |

| Withdrawal fee | Sending from an exchange | Fixed fees that hurt small deposits |

| Network fee | On-chain transfer | Congestion, fee tier you select |

| Conversion margin | Casino side | Quoted rate at credit or payout |

Volatility risk and stablecoins: when USDT or USDC reduces uncertainty

BTC and ETH can move hard between deposit and withdrawal. That changes your bankroll value even if you win.

- Use stablecoins for planning. USDT or USDC keeps your balance closer to a dollar value.

- Match the casino’s base currency. If the site settles in USD and you use a USD stablecoin, you cut conversion swings.

- Still check chain fees. Stablecoins can be cheap or expensive depending on the network.

Compliance realities: KYC, AML checks, and blockchain traceability

Crypto does not mean anonymous. Casinos and payment providers can screen funds.

- KYC still applies. Many casinos require ID before large withdrawals or any withdrawal.

- Source of funds checks happen. Deposits can trigger AML review based on patterns, size, or wallet risk flags.

- Blockchain is traceable. Your deposit address, withdrawal address, and transaction history can link together.

- Expect holds when something looks off. Reviews can slow payouts. Use this guide if you get blocked: Why was my casino withdrawal rejected?

Best practices: address safety, chain selection, and minimizing mistakes

- Pick the right network. Sending USDT on the wrong chain can burn your funds.

- Copy and paste the address. Do not type it. Do not trust screenshots.

- Check the first and last characters. Malware can swap addresses in your clipboard.

- Send a small test first. Use it when you deposit to a new casino or withdraw to a new wallet.

- Do not reuse deposit addresses across casinos. It reduces confusion and limits tracking links.

- Use your own wallet when possible. Exchange withdrawals can add delays and extra compliance checks.

- Keep transaction IDs. If support asks, you can prove the send and the exact time.

Country & Regulation Factors That Change the “Best” Method

Geographic availability changes your menu

Casinos do not offer one global cashier. They tailor options by country, state, and license.

- Local payment rails. Some regions rely on bank transfers and instant bank pay. Others push cards and e-wallets.

- Wallet coverage. Skrill, Neteller, PayPal, and local wallets vary by country. If a wallet cannot serve your region, the casino removes it.

- Crypto rules. Some markets limit crypto deposits, require extra source of funds checks, or block them fully.

- Withdrawal routing. Many casinos force you to withdraw to the same method you used to deposit. If that method cannot receive payouts in your country, you hit delays or method switches.

Legal markets vs offshore change the rails and your protections

Regulated casinos plug into approved processors. Offshore casinos often use alternate routing.

- Regulated markets. More stable banking support, clearer fees, and better dispute paths. You often get faster payouts once your account clears checks.

- Offshore markets. Higher chance of card declines, extra intermediaries, and processor changes. You see more third party merchant names and more failed attempts.

- Verification impact. Regulated sites enforce strict KYC before you withdraw. Offshore sites may delay KYC until payout time. Read the online casino KYC rules so you do not get stuck at cashout.

Banking restrictions and issuer policies cause “blocked” deposits

Your bank decides if a gambling transaction clears. The casino does not control that decision.

- MCC blocks. Many issuers block gambling merchant category codes by default. Some let you opt in, many do not.

- Cross border flags. Foreign acquiring banks and offshore processors trigger fraud rules. You get declines even with available funds.

- Credit vs debit. Credit cards often face more gambling limits than debit cards. Cash advance rules can add fees and interest.

- Name mismatch. If the merchant name on the statement looks unrelated, your bank may reject it or ask for extra authentication.

- Velocity rules. Multiple small attempts can look like fraud. One clean attempt works better than five retries.

Currency support decides your real cost

Speed and fees matter, but currency mismatch can cost more than both.

- Local currency support. If the casino supports your currency, you avoid forced conversion at deposit and withdrawal.

- Forced conversion. If the cashier shows only USD or EUR, you pay an FX spread. The casino, the processor, your bank, or all three can take a cut.

- Wallet base currency. Set your wallet base currency to match the casino account currency when possible. It reduces double conversion.

- Crypto pricing. Crypto deposits still involve FX in practice. You convert fiat to crypto, then the casino converts to its account currency or pegs to a rate.

Responsible gambling controls can limit methods and amounts

Regulators and operators can restrict how you fund your play.

- Deposit limits. Daily, weekly, and monthly caps can apply per method or across all methods. A “best” method becomes useless if you hit the cap.

- Cooling off. If you start a cooling off period, some casinos block deposits but still allow withdrawals.

- Self exclusion. Self exclusion can lock the cashier and prevent new deposits. You may need support to route withdrawals.

- Card and bank gambling blocks. Some banks offer gambling spending blocks. They can override casino settings and stop card payments and bank pay.

- Method removal. Some regulators restrict credit cards for gambling. In those markets, debit, bank transfer, and approved wallets win by default.

| Factor | What changes | What you should do |

|---|---|---|

| Region and license | Which methods appear, and which can withdraw | Check the cashier before you sign up, confirm withdrawal methods for your country |

| Regulated vs offshore | Processor stability, dispute options, KYC timing | Expect full KYC in regulated markets, avoid large deposits until you confirm payout flow |

| Issuer policy | Card approvals, cash advance fees, declines | Use debit or bank transfer if cards fail, avoid repeated retries |

| Currency mismatch | FX spreads, double conversion, worse rates | Match casino and wallet currency, avoid methods that force USD or EUR |

| RG controls | Deposit caps, blocked methods, enforced breaks | Set limits early, pick a method that still works under your caps |

How to Choose the Best Payment Method for Your Goals (Decision Framework)

Fastest withdrawals, prioritize rails that pay out 24/7

Your payout speed depends on two things. The casino’s approval time and the payment rail’s settlement time. You can only control the second part.

- Pick methods built for instant or same day payouts. E-wallets, instant bank transfer schemes, and real time bank rails usually clear fastest after approval.

- Match your deposit and withdrawal method. Many casinos force withdrawals back to the deposit method first. If you deposit by bank transfer, expect bank timing on the way out.

- Keep one primary method. Method switching triggers checks and slows approvals.

- Use a verified wallet or verified bank account. Unverified accounts cause manual review and delays.

- Avoid cards for withdrawals when you care about speed. Card withdrawals often run as reversals, can take days, and fail more often than bank or wallet payouts.

- Avoid weekend dependent methods. Some bank transfers pause or batch outside business hours.

If you want a deeper breakdown of timing by method and where delays happen, read online casino payout times explained.

Lowest fees, calculate total cost before you deposit

Do not compare only the headline fee. Compare the total cost of getting money in and out.

- Start with deposit fees. Casino fee plus provider fee. Some wallets charge on deposit, some do not.

- Add withdrawal fees. Many casinos advertise free withdrawals, but the provider can still charge. Banks can add receiving fees.

- Include FX spread and conversion count. The biggest hidden cost is exchange rate markup. Avoid double conversion, for example bank to USD to wallet to local currency.

- Check cash advance treatment on cards. Some issuers treat gambling deposits as cash advances. You pay a fee and immediate interest.

- Account for decline costs. Repeated card retries can trigger fraud controls. You lose time and sometimes get temporary blocks.

Simple total cost formula. Total cost = deposit fee + withdrawal fee + (FX rate you get vs mid market rate) + bank receiving or intermediary fees.

Higher limits, use a preparation checklist

Limits come from the casino, the provider, your bank, and your verification level. Raise the ceiling before you need it.

- Verify your identity early. Higher withdrawal limits often require full KYC. Upload documents before your first big win.

- Use a method that supports high per transaction limits. Bank transfer and some e-wallet tiers usually allow more than cards.

- Raise limits inside your wallet or bank. Many apps have daily caps you can adjust only after extra checks.

- Keep name and address consistent. Your casino profile, wallet, and bank account should match. Mismatches trigger manual review.

- Plan for source of funds checks. For larger cashouts you may need payslips, bank statements, or proof of deposits.

- Do not rotate methods. Multiple methods can split limits and increase compliance friction.

For a step-by-step approval guide, use how to verify your identity at an online casino.

More privacy, set realistic expectations

You cannot get full privacy at regulated casinos. You can reduce how much your bank sees, but you cannot avoid KYC when you withdraw.

- Best for bank statement privacy. E-wallets and prepaid vouchers can reduce direct casino entries on your bank activity.

- Trade-off you must accept. More privacy often means slower cashouts, lower limits, or fewer withdrawal options.

- Expect KYC on cashout. Even if you deposit with a voucher, casinos still verify you before paying winnings.

- Watch the fee stack. Privacy methods often add extra steps, each step can add fees or FX spread.

- Know your local rules. Some regions restrict certain wallets, prepaid products, or transfers for gambling.

If you play bonuses, avoid methods that may be excluded

Casinos often exclude some payment types from welcome offers, reloads, and free spins eligibility. They do it to manage fraud and fee costs.

- Commonly excluded. Prepaid vouchers, some e-wallets, and some mobile wallet routed payments can be ineligible at certain brands.

- Commonly accepted. Debit cards and bank transfers often qualify, but rules vary by casino and region.

- Check two lines before you deposit. The promo terms and the cashier page. Look for “eligible deposit methods” and “excluded payment methods”.

- Keep proof of deposit method. If support disputes eligibility, you want a clear transaction record.

Step-by-Step: Deposit and Withdraw Without Delays

Before You Deposit: KYC Readiness, Identity Matching, and Account Hygiene

- Finish KYC early. Upload ID and proof of address before your first deposit. Many casinos block withdrawals until you verify. Use current, readable documents. Avoid cropped images.

- Match your identity everywhere. Your casino profile name must match your payment account name. Use the same spelling, spacing, and middle initials. One mismatch can trigger manual review.

- Use one account. Do not open duplicates. Do not share devices or payment methods with friends or family. This often triggers fraud checks.

- Keep your contact details stable. Set your real address, phone, and email. Verify them if the casino offers it. Sudden changes look risky.

- Lock in two-factor security. Turn on 2FA where available. You cut login locks and payment holds. If you cannot sign in, use this guide on common sign-in fixes.

During Deposits: Prevent Errors With Names, Currencies, and Payment References

- Pick the right currency once. Choose your account currency before the first deposit. Changing it later can force withdrawals into a different method, or add conversion fees.

- Deposit with a method you can withdraw to. Many casinos require you to withdraw back to the same method, up to your deposit amount. If a method cannot receive withdrawals, expect extra steps.

- Do not mix methods mid-stream. If you deposit with cards, then switch to an e-wallet, you can trigger review. Keep one primary method until you complete your first withdrawal.

- Use correct bank references. For bank transfers, copy the reference exactly. Wrong or missing references cause unmatched payments and delays.

- Check limits before you hit confirm. Compare deposit minimum, maximum, and daily caps to your plan. Failed deposits often come from issuer limits, not the casino.

- Save proof. Keep the transaction ID, timestamp, and screenshots of success screens. You need them if support asks for evidence.

Withdrawal Workflow: Pending, Processing, and What “Approved” Means

- Requested. You submitted the cashout. The casino has not started checks yet.

- Pending. The casino holds the withdrawal for internal review. This is where KYC, bonus checks, and fraud screening happen.

- Processing. The casino approved the request and sent it to the payment provider. From here, delays often sit with banks, card networks, or e-wallet queues.

- Approved. The casino finished its part. It does not mean the money reached your account. You still wait for provider settlement times.

- Paid. The casino marked it completed. If you still do not see funds, check provider status and settlement windows, then contact support with the withdrawal ID.

Verification Triggers: Large Wins, Method Changes, and Unusual Activity Patterns

- Large withdrawals. Big cashouts often trigger enhanced checks. Expect extra documents and source of funds questions in some regions.

- Changing payment methods. Switching from card to e-wallet, or to a new bank account, can force fresh verification.

- Multiple failed deposits. Repeated declines can flag your account for risk review.

- Unusual location or device changes. Logging in from a new country, VPN, or many devices can trigger holds.

- Chargeback or dispute history. Any prior dispute with a card issuer can increase review time.

- Bonus abuse signals. High-risk patterns include rapid deposit, bonus claim, minimal play, then withdrawal. Casinos may ask for more checks before approval.

Troubleshooting Checklist: If a Deposit Fails or a Withdrawal Stalls

- If a deposit fails:

- Confirm your card or bank allows gambling transactions. Many issuers block them by default.

- Check your available balance and issuer daily limits.

- Match billing address and name to your bank records.

- Retry once. Do not spam retries. Multiple attempts can trigger blocks.

- Switch to a supported method that matches your verified identity, like bank transfer or an e-wallet, if available.

- Contact support with the transaction ID and error message.

- If a withdrawal stalls:

- Check status. If it is still pending, the casino has not released it.

- Confirm you completed KYC and your documents show “approved”, not “submitted”.

- Check bonus terms. Verify you met wagering and did not hit max cashout rules.

- Confirm your withdrawal method can receive funds in your region and currency.

- Do not change personal details during review. This can reset checks.

- Ask support for the exact hold reason and the next required step, in writing.

- Request a payment trace or ARN for card payouts, or a transfer reference for bank payouts, once marked paid.

Safety, Disputes, and Player Protection

What makes a payment method safe

A safe method proves it is you, blocks fraud, and logs every step.

- Authentication. Use methods with 2FA, app approval, biometrics, or 3D Secure for cards. Avoid methods that rely only on a password.

- Name matching. Your casino account name should match your payment account name. Mismatches trigger holds and manual reviews.

- Fraud controls. Look for device checks, velocity limits, and real time risk scoring. You see this as step up verification or a short security delay.

- Transaction monitoring. Strong providers flag unusual deposits, rapid reversals, and repeated failed attempts. This reduces account takeovers and card testing.

- Clear receipts. You should get an order ID, reference number, and timestamp for every deposit and cashout.

Chargebacks vs reversals vs refunds

These terms sound similar. They do not work the same way in gambling.

- Chargeback. A card dispute filed with your bank or card network. Many gambling deposits become hard to charge back once the casino proves delivery and play. Some banks still allow disputes for fraud or unauthorized use. Chargebacks can get your casino account restricted and can delay withdrawals during investigation.

- Reversal. A transaction that never fully settles. This usually happens fast, often the same day. You may see it after a failed authorization, a timeout, or a duplicate payment attempt.

- Refund. The merchant sends money back after settlement. Casinos often refund deposits back to the original method, especially when they reject your account, fail verification, or detect risk.

Keep evidence. Save receipts, confirmation emails, chat logs, and any payment trace or reference. Use the casino support route first. Escalate to the provider or bank only after you have a written timeline.

Protecting your identity

Reduce how many places hold your full banking and ID data.

- Use one primary wallet. An e wallet can limit how often you type card or bank details across casinos.

- Separate bankroll funds. Use a dedicated bank account or prepaid card for gambling spend. It limits exposure if credentials leak.

- Avoid sharing documents by email. Use the casino upload portal. If support asks for email, redact non required fields and send only what they request.

- Lock down your accounts. Enable 2FA on your email and wallet first. Most takeovers start at the inbox.

- Verify once, then stay consistent. Do not change address, phone, or name format during checks. If you need to verify, follow a tight process, see how to verify your identity at an online casino.

Spotting red flags

Bad payment flows cost you time and money. Watch for these signals.

- Predatory fees. High deposit fees, withdrawal fees, or “handling” charges with no schedule posted. Also watch FX markups that exceed typical provider spreads.

- Misleading processing times. “Instant withdrawals” that exclude verification, exclude weekends, or require a first time method test. Look for clear payout windows per method.

- Shady intermediaries. Unfamiliar merchants on your statement, multiple small debits instead of one deposit, or requests to send funds to a personal account. Legit casinos do not ask for person to person transfers to random names.

- Pressure tactics. Support pushes you to switch to crypto or gift cards to “fix” a delay. Treat this as high risk.

- Unclear limits. Missing max cashout rules, rolling limits, or method specific caps until after you request a withdrawal.

Data privacy considerations

Two parties store your data, the casino and the payment provider. Each keeps different records.

- What casinos store. Account profile data, KYC documents, deposit and withdrawal history, device and login logs, IP history, support tickets, and gameplay records tied to transactions.

- What providers store. Funding sources, transaction metadata, device data, fraud signals, chargeback history, and bank or card identifiers. Wallets also store merchant lists and payout destinations.

- What you should do. Use unique passwords, enable 2FA, and keep your funding sources minimal. If available, use a wallet that supports tokenized card storage and merchant specific approvals.

| Risk | What it looks like | What you do |

|---|---|---|

| Account takeover | New device logins, password reset emails, failed 2FA prompts | Secure email first, change passwords, enable 2FA, freeze withdrawals with support |

| Hidden costs | Extra processor fees, bad FX rates, “service” charges | Check fee tables, test with a small deposit, avoid forced currency conversion |

| Payment routing issues | Different merchant names, split transactions, repeated pending states | Stop retries, collect references, ask for trace details, escalate with proof |

Best Options by Scenario (Recommended Shortlists)

Best for beginners, simple setup and high acceptance

- Debit card, fast setup, widely accepted, instant deposits. Watch cash advance flags and bank blocks.

- Instant bank transfer, high approval rates, no card checks, usually quick deposits. Confirm your name matches your bank profile.

- PayPal, simple login, strong acceptance where offered, quick deposits. Some casinos limit withdrawals to the same PayPal account.

- Apple Pay or Google Pay, quick checkout, fewer input errors, good acceptance on mobile. Behind the scenes it can still route as a card.

Start with one method you can use for both deposits and withdrawals. Make a small test deposit first. Save screenshots of the cashier confirmation and transaction ID.

Best for frequent cashouts, optimized for repeat withdrawals

- E-wallets (Skrill, Neteller), fast withdrawals at many casinos, clean transaction history, easy repeat cashouts. Fees can add up, check wallet withdrawal fees.

- Bank transfer, reliable for regular withdrawals, fewer reversals. Slower than wallets but steady.

- Crypto (USDT, BTC, ETH), fast once approved, works well for frequent payouts. Confirm network and token before you send.

Keep your KYC current. Use the same method every time. Avoid switching wallets mid stream, it triggers reviews. If speed matters most, read online casino payout times explained before you commit.

Best for big bankrolls, higher limits and fewer interruptions

- Bank transfer, best for large amounts, fewer hard caps, clear source of funds trail. Expect extra checks on first big withdrawal.

- Crypto, high ceiling at many sites, fewer banking limits. Volatility risk if you hold coins.

- Premium e-wallet tiers, higher limits after verification, faster handling. You still pay wallet fees.

Best for travel and multi-currency players, minimize conversion losses

- Multi-currency e-wallet, hold balances in several currencies, convert when rates suit you. Watch wallet FX spreads.

- Crypto stablecoins (USDT, USDC), reduce FX exposure, consistent value for transfers. Confirm the casino supports the exact coin and network.

- Local bank transfer rails, lower fees in-region, fewer declines than foreign cards. Coverage depends on your country.

Avoid forced conversion at checkout. If the cashier offers DCC, decline it and pay in the casino account currency when possible.

Best for responsible budgeting, enforce spending control

- Prepaid vouchers (PaysafeCard), you can only spend what you buy, no bank link. Often deposit only, withdrawals usually go to bank or wallet.

- Dedicated debit card for gambling, isolate spending, set bank level limits, easy tracking. Some banks still block gambling MCCs.

- E-wallet with strict limits, set top-up caps, lock funding sources, separate casino from your main bank. Fees can punish small frequent deposits.

- Instant bank transfer with low daily caps, good control if your bank supports tight limits. Approval varies by provider.

Pick one method that supports your limits. Turn on 2FA. Set deposit caps in your wallet or bank first, then match them inside the casino.

FAQ

What is the cheapest online casino payment method?

Instant bank transfer often has the lowest fees. Many casinos charge 0% on deposits and withdrawals, but your bank or provider may add a small fee. Cards can add cash advance fees. Some e-wallets add FX and withdrawal fees.

What payment method is fastest for withdrawals?

E-wallets and instant bank transfer usually pay out fastest after approval. Cards often take longer due to card network processing. Crypto can be fast on-chain, but casino approval still controls start time. Always check the casino withdrawal processing window.

Why do some methods work for deposits but not withdrawals?

Casinos follow closed-loop rules. They send funds back to the source you used to deposit. Some deposit tools, like prepaid vouchers, cannot receive payouts. In that case, you must add a payout method, usually bank transfer or e-wallet.

Do online casinos charge fees on deposits or withdrawals?

Many casinos list 0% fees, but third parties can still charge you. Watch for card cash advance fees, e-wallet withdrawal fees, bank transfer fees, and FX spreads. Read the cashier fee note and your provider fee schedule before you deposit.

What limits should you expect for deposits and withdrawals?

Limits depend on the method and your verification level. Cards and wallets often cap single transactions. Bank transfer can allow higher payouts but may have higher minimums. High rollers hit daily limits first. Set caps in your wallet or bank, then in-casino.

Do you need KYC to withdraw?

Yes in most cases. Casinos usually require ID checks before the first withdrawal or when you hit volume thresholds. Match the name on your payment method to your casino account. Upload documents early to avoid delays when you request a payout.

Which method is best for strict bankroll control?

Prepaid vouchers and dedicated e-wallets work well. You can set fixed top-ups, separate gambling funds from your main bank, and stop funding fast. Avoid credit cards if you want hard limits. Use 2FA on your wallet and casino account.

How do you avoid withdrawal delays?

Use one deposit method, then withdraw to the same method when possible. Complete KYC before you request a payout. Avoid bonus terms that add wagering. Keep your account details consistent. For timelines, see online casino payout times.

Is crypto better than cards or bank transfer?

Crypto can reduce banking friction and may speed up transfers. It can also add network fees and price swings. Some casinos apply higher minimums or extra checks. Use stablecoins if offered. Confirm supported networks to avoid costly wrong-chain transfers.

Can you use Apple Pay, Google Pay, or PayPal at casinos?

Availability depends on your country, state, and the casino’s processor. These options often work for deposits, but withdrawals may route to bank transfer or wallet rails. Check the cashier list before you register, not after you win.

Conclusion

Conclusion

Pick your payment method based on three numbers. Total fees, payout speed, and your daily limits.

Cards work for fast deposits, but you often lose on withdrawals. Bank transfer gives higher limits, but slower cashouts. E-wallets and instant bank rails usually balance speed and cost. Crypto can be fastest, but only if the casino supports the right network and you handle address checks.

- If you want the quickest withdrawals: use the same wallet or instant bank method for deposits and cashouts.

- If you want fewer payout issues: verify early, match your account name, and keep one method on file.

- If you want lower total cost: avoid methods with hidden FX rates, conversion fees, and cash-advance coding.

- If you use crypto: send a small test transfer first, then move the full amount.

Before you deposit, open the cashier page. Check supported deposit and withdrawal rails, minimums, maximums, and processing times. If the casino requires verification, finish it first. Use this KYC guide and keep your documents ready.

-

Online Casino KYC Explained: Verification Process, ID Checks, Age Rules & AML

4 months ago -

How to Sign Up & Create an Online Casino Account (Step-by-Step)

4 months ago -

How to Verify Your Identity at an Online Casino (and Get Approved Faster)

4 months ago -

How to Withdraw Money from an Online Casino: Methods, Steps & Tips

4 months ago -

Online Casino Payout Times Explained: How Long Withdrawals Take (and Why)

4 months ago

-

- Card Payments (Visa, Mastercard, AmEx): Fast Deposits, Variable Withdrawal Experience

- Why card deposits get declined: issuer blocks, MCC codes, and fraud rules

- Fees to watch: cash-advance treatment, international charges, and FX conversion

- Withdrawal realities: push-to-card availability and alternative cashout routes

- 3D Secure and chargebacks: what they mean for player safety and disputes

- Best practices: reducing declines and improving approval rates

-

- How vouchers work for deposits, and why withdrawals use a different method

- Fees and limits, activation, redemption, and caps

- Privacy and control, tighter budgeting with less bank exposure

- Common friction points: availability, region rules, and KYC triggers

- Best use cases: deposit-only play and bankroll management

-

- Cryptocurrency Payments (BTC, ETH, USDT, and Altcoins)

- Transaction lifecycle: confirmations, mempool congestion, and real-world timing

- True cost comparison: exchange spreads, wallet fees, and network gas fees

- Volatility risk and stablecoins: when USDT or USDC reduces uncertainty

- Compliance realities: KYC, AML checks, and blockchain traceability

- Best practices: address safety, chain selection, and minimizing mistakes

-

- Before You Deposit: KYC Readiness, Identity Matching, and Account Hygiene

- During Deposits: Prevent Errors With Names, Currencies, and Payment References

- Withdrawal Workflow: Pending, Processing, and What “Approved” Means

- Verification Triggers: Large Wins, Method Changes, and Unusual Activity Patterns

- Troubleshooting Checklist: If a Deposit Fails or a Withdrawal Stalls

-

- What is the cheapest online casino payment method?

- What payment method is fastest for withdrawals?

- Why do some methods work for deposits but not withdrawals?

- Do online casinos charge fees on deposits or withdrawals?

- What limits should you expect for deposits and withdrawals?

- Do you need KYC to withdraw?

- Which method is best for strict bankroll control?

- How do you avoid withdrawal delays?

- Is crypto better than cards or bank transfer?

- Can you use Apple Pay, Google Pay, or PayPal at casinos?

-

- Card Payments (Visa, Mastercard, AmEx): Fast Deposits, Variable Withdrawal Experience

- Why card deposits get declined: issuer blocks, MCC codes, and fraud rules

- Fees to watch: cash-advance treatment, international charges, and FX conversion

- Withdrawal realities: push-to-card availability and alternative cashout routes

- 3D Secure and chargebacks: what they mean for player safety and disputes

- Best practices: reducing declines and improving approval rates

-

- How vouchers work for deposits, and why withdrawals use a different method

- Fees and limits, activation, redemption, and caps

- Privacy and control, tighter budgeting with less bank exposure

- Common friction points: availability, region rules, and KYC triggers

- Best use cases: deposit-only play and bankroll management

-

- Cryptocurrency Payments (BTC, ETH, USDT, and Altcoins)

- Transaction lifecycle: confirmations, mempool congestion, and real-world timing

- True cost comparison: exchange spreads, wallet fees, and network gas fees

- Volatility risk and stablecoins: when USDT or USDC reduces uncertainty

- Compliance realities: KYC, AML checks, and blockchain traceability

- Best practices: address safety, chain selection, and minimizing mistakes

-

- Before You Deposit: KYC Readiness, Identity Matching, and Account Hygiene

- During Deposits: Prevent Errors With Names, Currencies, and Payment References

- Withdrawal Workflow: Pending, Processing, and What “Approved” Means

- Verification Triggers: Large Wins, Method Changes, and Unusual Activity Patterns

- Troubleshooting Checklist: If a Deposit Fails or a Withdrawal Stalls

-

- What is the cheapest online casino payment method?

- What payment method is fastest for withdrawals?

- Why do some methods work for deposits but not withdrawals?

- Do online casinos charge fees on deposits or withdrawals?

- What limits should you expect for deposits and withdrawals?

- Do you need KYC to withdraw?

- Which method is best for strict bankroll control?

- How do you avoid withdrawal delays?

- Is crypto better than cards or bank transfer?

- Can you use Apple Pay, Google Pay, or PayPal at casinos?

-

Reload Bonus Explained: What It Is and When It’s Worth Claiming

1 month ago -

Online Casino Licensing Explained: Authorities, Licenses & How to Check One

3 months ago -

Best Live Dealer Casinos: Where to Play Live Blackjack, Roulette & More

3 months ago -

Best Online Casinos for High Rollers: VIP Perks, High Limits & Exclusive Bonuses

3 months ago -

Fast Payout Online Casinos: Best Sites for Quick Withdrawals

3 months ago

-

Online Casino Licensing Explained: Authorities, Licenses & How to Check One

3 months ago -

Are Online Casinos Legal? Complete Guide by State & Country

4 months ago -

Casino VIP & Loyalty Programs Explained: Points, Tiers, Rewards & Rakeback

4 months ago -

Online Casino Fairness Explained: RNG, RTP, House Edge & Provably Fair

4 months ago -

Free Spins Bonus Explained: How Free Spins Work at Online Casinos

4 months ago