How to Set a Gambling Budget (That You’ll Actually Stick To)

A gambling budget protects your rent money. It protects your time. It also keeps losses from turning into debt.

In 2024, a NerdWallet survey found sports bettors said they spent an average of $3,284 on gambling. If you do not set limits, your spending can drift fast.

This guide shows you how to set a gambling budget you can follow. You will learn how to calculate disposable income, pick a monthly limit, split it into session caps, and set stop rules for losses and time. You will also learn how to track results and adjust without chasing.

If you struggle to keep to limits, read these problem gambling signs before you bet again.

Key Takeaways

- In het kort: Base your gambling budget on disposable income, not your total income.

- In het kort: Set one fixed monthly limit and treat it as a cost, not an investment.

- In het kort: Keep the limit small, many guides use 1 to 5 percent of disposable income as a guardrail.

- In het kort: Split your monthly budget into session caps, decide the amount before you play.

- In het kort: Use hard stop rules for loss and time, stop when you hit either limit.

- In het kort: Track every deposit, withdrawal, and net result, use one simple log.

- In het kort: Do not use wins to raise limits, roll them into next month or cash them out.

- In het kort: Adjust the budget only after a full month, never after a losing session.

- In het kort: Check that your site is regulated before you deposit, use this guide to check a casino license.

A 2024 NerdWallet survey reported average annual gambling spend of $3,284. Use that number as a warning signal, not a target. Your budget must fit your bills, debt payments, and savings first.

What a Gambling Budget Is (and What It Isn’t)

Budget vs. bankroll vs. loss limit

People mix up three terms. They are not the same.

| Term | What it is | What it is not |

|---|---|---|

| Gambling budget | The total amount you allow yourself to spend on gambling for a set period, usually a month. | A goal to “win back” money. A number you change after a bad night. |

| Bankroll | The money you set aside from your budget to play with right now, often split by game or week. | Your full bank balance. Money meant for bills or savings. |

| Loss limit | A hard stop for how much you can lose in a session, day, or week. | Your full budget. A “suggestion” you ignore when you feel confident. |

Your budget sets the ceiling. Your bankroll is what you bring to play. Your loss limit is the stop sign.

Entertainment spend mindset

Treat gambling like paid entertainment. You pay for time and excitement.

Do not treat your budget as an investment. Most players lose over time. The house edge and fees do the work.

A 2024 NerdWallet survey reported average annual gambling spend of $3,284. Use it as a risk marker. If your spend trends toward that number, check your totals and cut back.

The #1 rule: never use rent, bills, debt, or emergency money

Fund gambling only with money you can afford to lose. That means money left after:

- Rent or mortgage.

- Utilities, food, transport, insurance.

- Minimum debt payments, plus your payoff plan.

- Emergency fund contributions.

If you cannot cover those first, your gambling budget is zero. Pause gambling. Use responsible gambling tools to block deposits, set limits, or take a break.

Who this guide is for

This guide fits any gambling where money leaves your account fast.

- Online casinos, slots and table games.

- Sports betting, pregame and live betting.

- Poker, cash games and tournaments.

- Other online gambling, including betting apps and hybrid products.

The games differ. The budget rule stays the same. Set a monthly cap. Split it into smaller limits. Stop when you hit them.

Why Most People Fail to Stick to a Gambling Budget

The psychology of chasing losses and tilt

Your brain treats losses as problems to fix. Gambling offers a fast, familiar “fix” button. You bet again to get back to even.

After a loss, stress rises. Your decision quality drops. You raise stakes, speed up play, or widen the types of bets you place. Many players call this tilt. The result is simple. You break your limits when you need them most.

Chasing also changes your goal. You stop following your budget. You focus on one outcome, getting your money back. That goal pushes you into higher risk bets and longer sessions.

House edge, variance, and why short-term wins can be misleading

The math stays the same even when you feel “hot.” In most casino games, the house edge means the expected result over time is a loss.

Variance hides that reality in the short run. You can win today and still lose over a month. You can lose five sessions in a row and still be close to the expected result.

Short-term wins create a dangerous budget story. You start to treat wins as proof of skill. You raise your limits because “it’s working.” This is how a budget turns into a moving target.

- House edge pushes your long-term result negative.

- Variance creates streaks that feel meaningful but often are not.

- Early wins increase confidence and bet size, which increases losses when the swing reverses.

Banking friction: how easy deposits sabotage willpower

Budgets fail when deposits feel painless. One-click top ups, saved cards, e-wallets, and instant bank transfers remove the pause that protects you.

Speed matters. If you can reload in seconds, your “stop point” disappears. You hit your limit, then you buy a new limit.

Prompts make it worse. Apps push reload buttons, bonus offers, and “recommended” deposit sizes. Your budget has to compete with a product designed to keep you playing.

If you need a hard stop, use tools that block access, including online casino self-exclusion.

Cognitive traps: sunk cost fallacy, gambler’s fallacy, and “one more bet” thinking

Three thinking errors break most budgets.

- Sunk cost fallacy: You already spent time and money, so you keep going to “make it worth it.” Your past losses cannot improve your next odds.

- Gambler’s fallacy: You believe a win is “due” after losses, or a loss is “due” after wins. Each bet stands alone in games of chance.

- “One more bet” thinking: You treat the next bet as a small exception. Small exceptions stack fast. They erase your cap.

These traps share one pattern. They turn a fixed budget into a negotiation. If you keep negotiating, the budget loses.

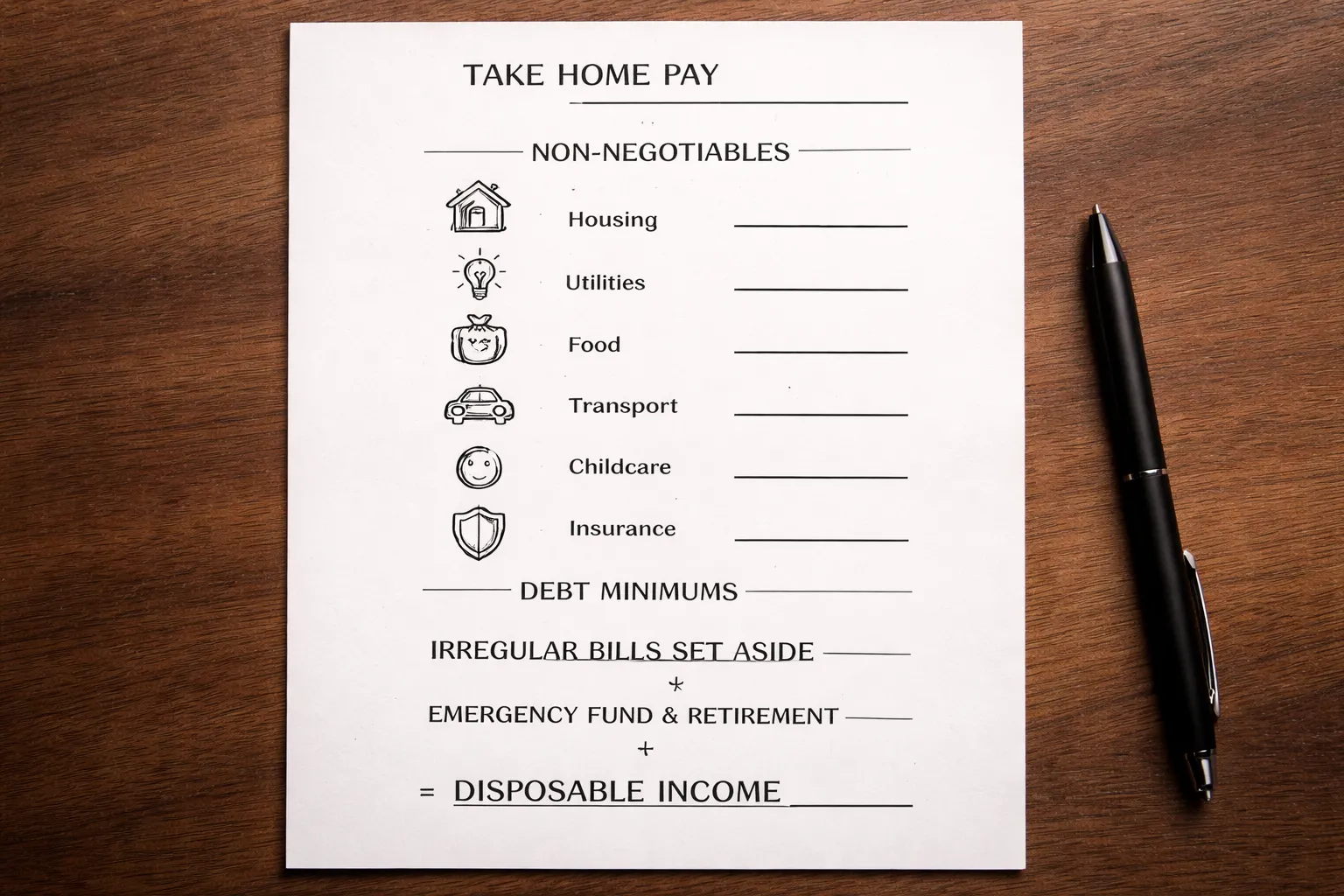

Step 1: Calculate Your True Disposable Income

Step 1: Calculate Your True Disposable Income

Your gambling budget comes from one place. Money you can lose without touching bills, debt, or savings goals. That number is your true disposable income.

List your non negotiables first

Start with the costs that keep your life running. Treat these as fixed. Do not fund gambling until these get covered.

- Housing: rent or mortgage, property tax, HOA fees

- Utilities: electric, gas, water, trash, phone, internet

- Food: groceries, basic household supplies

- Transport: fuel, transit pass, parking, maintenance

- Childcare: daycare, after school care, babysitting needed for work

- Insurance: health, auto, renters or homeowners, life if required

Add debt minimums and irregular expenses

Minimum debt payments are non negotiable. Missing them creates fees, interest spikes, and credit damage.

- Debt minimums: credit cards, personal loans, student loans, auto loan, buy now pay later

Next, capture bills that hit quarterly or yearly. If you ignore them, you will borrow from your gambling money later.

- Annual and quarterly bills: car insurance paid every 6 months, subscriptions, professional dues, vehicle registration, tax payments, school fees

- Predictable repairs: tires, brakes, appliance replacement, basic medical and dental costs

Convert irregular costs into a monthly number. Take the annual total, divide by 12. Do the same for quarterly bills, divide by 3.

Pay yourself first, emergency fund and retirement

Set your savings targets before you set any gambling cap. This reduces the chance you treat gambling as a fallback plan.

- Emergency fund: build to 3 to 6 months of core expenses. Start with a small automatic transfer if you are at zero.

- Retirement: contribute enough to get any employer match. If you have no match, pick a fixed monthly amount you can sustain.

Use a simple disposable income formula

Disposable income = monthly take home pay minus non negotiables minus debt minimums minus irregular bills set aside minus emergency fund contribution minus retirement contribution.

- Take home pay: $3,500

- Housing: $1,350

- Utilities: $250

- Food: $450

- Transport: $300

- Insurance: $250

- Childcare: $0

- Debt minimums: $300

- Irregular bills set aside: $150

- Emergency fund: $100

- Retirement: $175

- Total essentials and goals: $3,325

- True disposable income: $3,500 minus $3,325 equals $175

If your disposable income is $175, your gambling budget cannot exceed $175 for the month. Anything above that comes from bills, debt, or savings. That is how budgets break.

When disposable income is $0

If your disposable income is zero, your gambling budget is zero. Do not negotiate it. Use safer options until your cash flow improves.

- Pause deposits and set hard limits using responsible gambling tools

- Choose free entertainment, free to play games with no deposits, streaming, library, community events

- Switch the urge into a fixed cost habit, short walk, workout, cooking, a call with a friend

- Track spending daily for 14 days, cut one recurring cost, then rebuild a small emergency buffer

- If gambling already creates bill stress, use self exclusion and get support from a local or national helpline

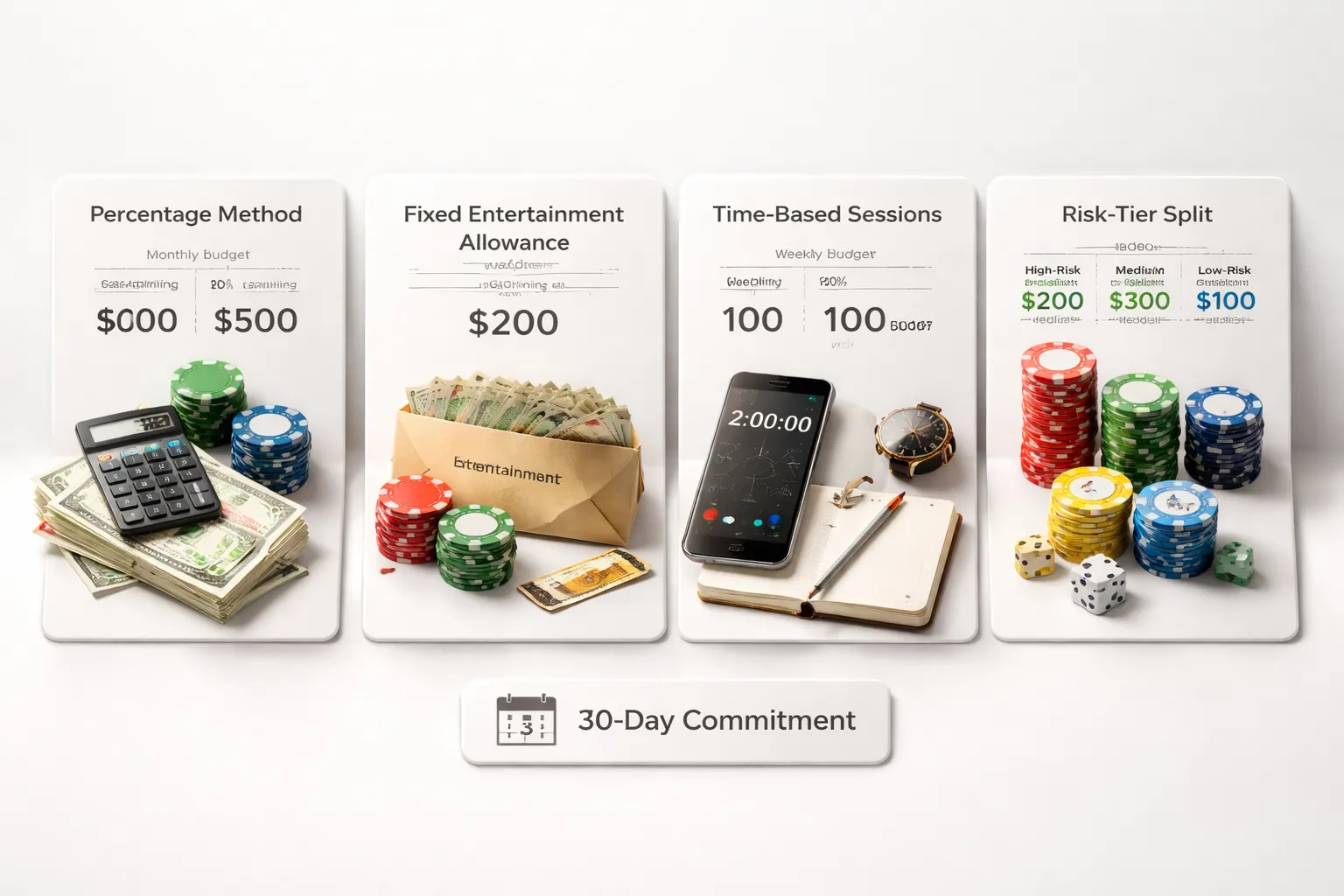

Step 2: Choose a Budgeting Method You’ll Actually Follow

Step 2: Choose a Budgeting Method You’ll Actually Follow

Pick one method. Write it down. Use it for 30 days. If you change methods every week, you will break your own rules.

Percentage method (1% to 5%)

This method sets your gambling budget as a small percent of your take home pay.

- How to set it: Choose a percent, then multiply by your monthly take home income. Example, 3% of $3,000 equals $90 per month.

- When it works: Your income is stable. Your bills are current. You want a simple rule that scales with your pay.

- When it fails: Your income swings. You use gambling to chase losses. You already feel bill pressure. A percent can still be too high if you have debt, late fees, or no emergency buffer.

- Hard rule: If you carry balances at high interest, start at 0% until you build a buffer and stop the bleeding.

Use a cap. Percent based budgets can grow fast. Many people underestimate what they spend. A 2024 NerdWallet survey found people said they spent an average of $3,284 on gambling that year. That is about $274 per month.

Fixed entertainment allowance

This method treats gambling like movies, dining out, or subscriptions. You set one fixed number and keep it the same each month.

- How to set it: Choose a dollar amount you can lose without stress. Put it on a separate card, prepaid card, or a separate account.

- Keep it stable: Do not raise it after a win. Do not top it up after a loss. If you want to change it, do it only on a set date, like the first of next month.

- Best use case: You want predictability. You tend to overspend when you have access to more cash.

- Watch for: “Just this once” deposits. Those are budget leaks. Treat them as a rule break, not a small exception.

Time based method (hours or sessions)

This method limits how long you play. You still set a money cap, but you manage your risk by cutting exposure time.

- How to set it: Decide sessions per week and minutes per session. Example, 2 sessions per week, 45 minutes each. Set an alarm. Stop when it rings.

- Add a money ceiling: Use a fixed loss limit per session. Time limits alone do not stop overspending.

- When it works: You spiral when you play too long. You lose track of time. You play late at night.

- When it fails: You play faster under time pressure. You increase bet size to “make the session count.” If you do that, switch to a fixed allowance method.

Risk tier method (low risk vs high risk)

This method splits your budget based on how volatile the game is and how you behave when you play it.

- Set two buckets: Low risk play and high risk play. Low risk gets most of the budget.

- Example split: 80% low risk, 20% high risk.

- Low risk bucket: Small stakes. Slower pace. Lower maximum bet. One deposit only.

- High risk bucket: High volatility slots, live betting, parlays, rapid games. This bucket needs a tight cap and fewer sessions.

- Why it works: You stop one bad night from wiping out the whole month.

If you gamble online, also check that you play on licensed sites with clear limit tools and account controls. Use a quick license check before you deposit.

Quick self check: match the method to your personality and triggers

If any method keeps collapsing, add friction. Remove saved cards. Lower deposit limits. Use cooling off or exclusion tools. If you need a stronger reset, read how self exclusion works and what happens next.

Step 3: Set Layered Limits (Monthly, Weekly, Session, and Deposit Caps)

Monthly cap: your non-negotiable ceiling

Start with one number. Your monthly cap. This is the maximum you will allow yourself to lose in a month.

Set it from your fixed allowance. Do not raise it because you had a good week. Do not raise it to chase a bad one.

- Make it hard to break: set a platform deposit limit at or below this number.

- Use one funding source: one card or one e wallet. No backups.

- Track against the cap: log deposits and withdrawals. Do not rely on memory.

Weekly and per-session caps: stop one bad night

Monthly limits fail when you burn the budget in a weekend. Add smaller caps that force pauses.

- Weekly cap: set at 20 to 30 percent of your monthly cap. If you hit it, you stop until next week.

- Session cap: set at 5 to 10 percent of your monthly cap. If you hit it, you end the session.

- One session per day: no reload sessions later the same day.

Example. Monthly cap $200. Weekly cap $50. Session cap $20. That structure blocks a single run from wiping out the month.

Deposit limits vs. loss limits vs. wager limits: know what each controls

Platforms offer different limit types. They do different jobs. Use more than one.

| Limit type | What it controls | What it does not control | Best use |

|---|---|---|---|

| Deposit limit | How much money you can add in a day, week, or month | How fast you can lose what is already in your account | Stops reload behavior and chasing with new money |

| Loss limit | Maximum net loss over a period | How long you play, how large each bet is | Ends play when results go against you |

| Wager limit | Total amount you can stake over a period | Your net loss, because you can recycle wins into more bets | Controls high volume betting and fast games |

Set a deposit limit first. Then add a loss limit. Add a wager limit if you play fast cycle games or you keep increasing bet size.

If you cannot find these tools, treat that site as higher risk. Check the operator and regulator details using this casino licensing guide.

Time limits and break rules: stop fatigue decisions

Money limits do not stop tilt. Time limits do.

- Session timer: 30 to 60 minutes for casino games. 60 to 120 minutes for sports research and placing bets.

- Hard stop rule: when the timer ends, you cash out or close the app. No last bet.

- Break rule: after any loss streak or any big win, take a 15 minute break. Leave the screen.

- Stop on first break if you chase: once you need a break, you end the day.

Cash-only or preloaded card for in-person gambling

In person gambling gets risky when you have access to more cash. Remove access.

- Cash-only: bring your session cap in cash. Leave cards at home.

- Preloaded card: load your weekly cap before you go. Do not reload on site.

- No ATM rule: do not use venue ATMs. If you withdraw once, you go home.

- Separate travel money: keep transport and food money separate from gambling cash.

Layered limits work because they force stops at multiple points. Monthly protects your finances. Weekly protects your month. Session protects your night. Deposit caps protect you from yourself.

Step 4: Decide How Much to Bet Per Wager (Unit Sizing)

Step 4: Decide How Much to Bet Per Wager (Unit Sizing)

Use a “unit” to control variance

A unit is your standard bet size. You set it once, then you bet in units.

This protects you from variance. Variance means normal losing streaks that happen even when you make decent picks. If your bets swing in size, variance hits harder. If your bets stay consistent, you stay in control.

Unit sizing also makes your results easier to track. You measure wins and losses in units, not emotions.

Rule-of-thumb unit sizes

Pick a unit that fits your bankroll and your game type.

- Sports betting: 1% to 2% of your bankroll per wager. Use 1% if you tilt, chase, or bet often. Use 2% only if you stay disciplined.

- Casino-style wagering (slots, roulette, fast games): 0.25% to 1% of your bankroll per bet. Faster games create more swings per hour, so you need smaller units.

If your unit feels “too small to matter,” keep it anyway. The goal is to last long enough to follow your session cap, not to force action.

Do not double after losses

Doubling stakes after a loss can blow up your bankroll fast. It turns a normal downswing into a budget failure.

The math is simple. Each double increases your required bet size and your exposure. A short losing streak can push you into bets you never planned to place. Then your layered limits break.

Do this instead.

- Use fixed units. No exceptions.

- If you feel the urge to chase, stop betting for the session.

- If you still want structure, use a pre-set stake ladder that never increases after losses. Example, 1 unit flat, or 1 unit then 0.5 unit, then stop.

If you use online play, set limits inside your account so you cannot override your plan in the moment. See responsible gambling tools for deposit and loss controls.

Simple examples: $200 bankroll vs. $1,000 bankroll

| Bankroll | Sports unit (1%) | Sports unit (2%) | Casino unit (0.5%) | Casino unit (1%) |

|---|---|---|---|---|

| $200 | $2 | $4 | $1 | $2 |

| $1,000 | $10 | $20 | $5 | $10 |

Now connect unit size to your session cap. If your session cap is $50 and your unit is $5, you have 10 units for the session. When they are gone, you stop. No top-ups.

When advanced staking is a bad idea

Systems like Kelly sizing can look “optimal” on paper. Most gamblers should avoid them.

- They require accurate odds and accurate win probability estimates. Most people do not have them.

- They increase bet size after wins. That can raise your risk right when you feel confident.

- They create bigger swings. Bigger swings make it harder to stick to session and weekly limits.

If your main goal is budget control, use a flat unit. Keep it boring. Boring is how you stay inside your limits.

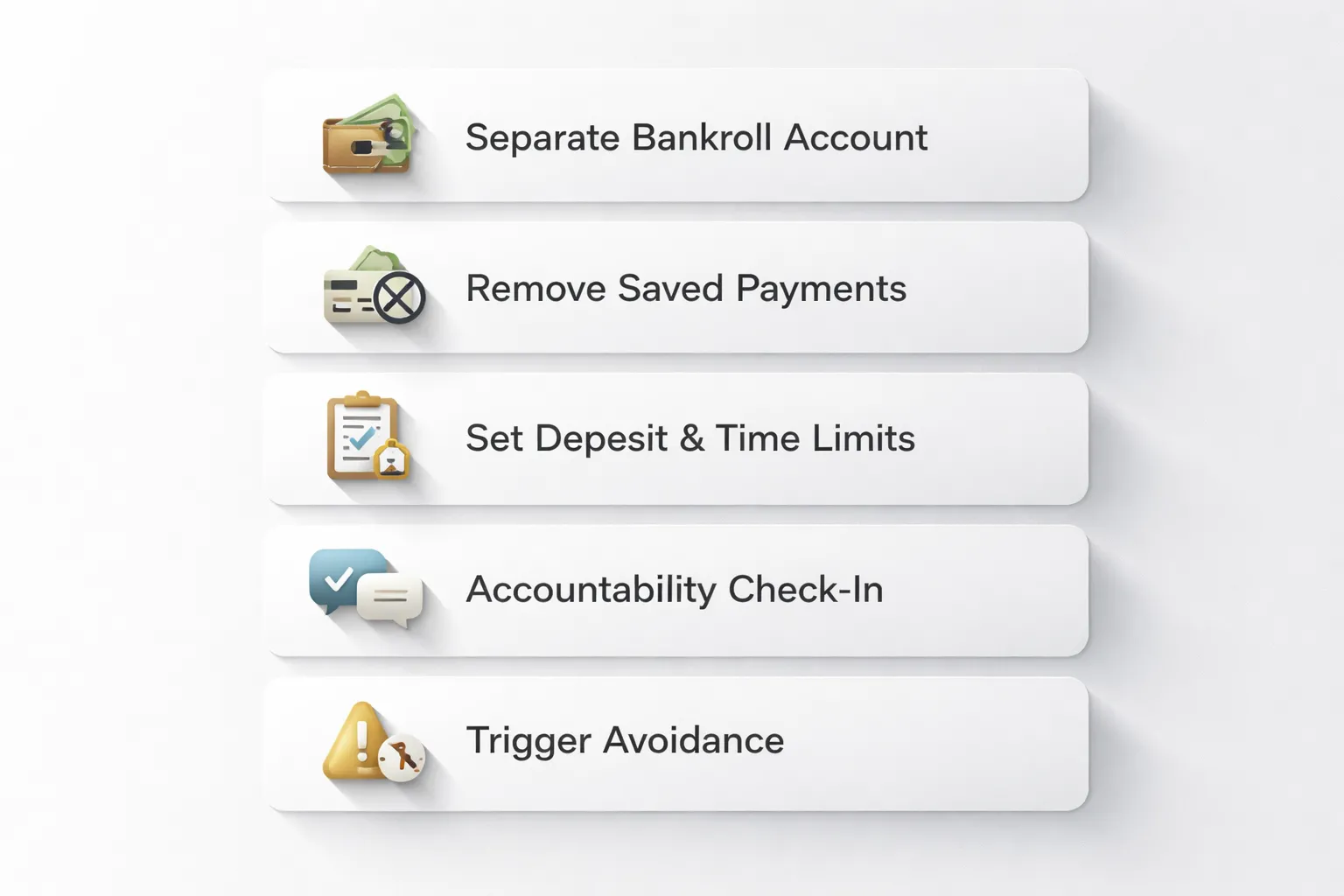

Step 5: Build Guardrails That Make Overspending Hard

Separate accounts

Keep gambling money away from your daily money. Use a dedicated e-wallet or a separate bank account. Move in only what you planned for the week or month. Do not top up mid-session.

- One account, one purpose. Bills and savings never touch this balance.

- Pre-load on a schedule. Weekly works better than monthly for most people.

- Withdraw wins out. Sweep profits to your main account on a set day.

Remove frictionless funding

Fast deposits break budgets. Add steps that slow you down.

- Unlink debit and credit cards from gambling sites.

- Disable one-click deposits and saved payment methods.

- Turn off instant bank transfers inside gambling apps if you can.

- Block cash advances on your credit card. Ask your issuer to do it.

- Keep your bankroll account off your phone. Access it only from a desktop.

Use platform tools

Set limits before you play. Limits set mid-session fail more often.

- Deposit limits. Set daily and weekly caps. Pick numbers you can live with. Keep them below your budget so you have a buffer.

- Loss limits. If your site offers them, use them. Match them to your session limit.

- Time limits. Cap session length. Long sessions drive higher spend.

- Cool-off periods. Use 24 hours when you feel tilt, stress, or urgency.

- Self-exclusion. Use it when you cannot stick to limits. Make it long enough to matter. Learn the details in this self-exclusion guide.

Accountability tactics

You follow rules better when someone else can see them.

- Pick a check-in partner. Share your weekly limit and your actual spend. Send one screenshot per week.

- Use shared tracking. A simple sheet with date, deposits, withdrawals, and net result. No stories. Just numbers.

- Set a permission rule. You ask your partner before any extra deposit. If you already deposited your limit, the answer stays no.

Environment design

Cut triggers that lead to extra bets. Reduce access. Reduce exposure.

- Delete gambling apps from your phone. Use browser access only, or do not access at all.

- Turn off push notifications, promo emails, and SMS offers.

- Avoid late-night play. Fatigue lowers control and raises spend.

- Do not gamble while drinking. Alcohol weakens limit compliance.

- Avoid venues that pull you in, especially after work or after losses.

- Do not chase bonuses. Bonus deadlines push rushed deposits.

| Guardrail | What you do | Why it works |

|---|---|---|

| Separate bankroll account | Fund it once per week | Stops bill money from becoming betting money |

| Remove saved payments | Unlink cards, disable one-click | Adds delay before an impulse deposit |

| Deposit and time limits | Set before play | Blocks overspending when emotions spike |

| Check-in partner | Share weekly numbers | Raises follow-through |

| Trigger control | No alcohol, no late-night, no promos | Removes common overspend cues |

Tracking and Review: Make Your Budget Adaptive, Not Emotional

What to Track: The Numbers and the Triggers

If you do not track it, you will guess. Guessing feeds emotion. Track six items after every session.

- Deposits: Total added to your account. This shows how often you “top up.”

- Net loss: Money in minus money out. Use withdrawals, not “balance.”

- Session length: Start time and end time. Long sessions raise risk.

- Game types: Slots, live casino, sports, poker. Your risk profile changes by game.

- Stake size: Your typical bet and your highest bet. Spikes flag tilt.

- Emotions: One word before and after. Calm, bored, angry, stressed, hyped.

Simple Tracking Templates: One Sheet, One Routine

Use a basic spreadsheet. Keep it boring. Boring works.

- Date

- Platform

- Game type

- Deposit

- Withdrawals

- Net result

- Session minutes

- Average stake

- Max stake

- Emotion before

- Emotion after

- Notes

Run a weekly review. Same day, same time. No exceptions.

- Add up deposits and net losses for the week.

- List your three longest sessions.

- Mark any session with max stake above your normal range.

- Count sessions that started with stress, anger, or boredom.

- Write one rule for next week. Keep it specific.

Set a Review Cadence: Adjust Monthly Only

Do not change your budget after a win. Do not chase after a loss. Both moves come from emotion.

Make budget changes once per month. Use your tracking data, not your memory.

- If you stayed within limits for four weeks, you can keep the same budget.

- If you broke limits even once, tighten controls. Lower deposit limits. Shorten session caps.

- If gambling started to bleed into essentials, pause play and set stricter barriers. Use responsible gambling tools to enforce it.

How to Handle Wins Responsibly: Withdraw First

Wins create permission to overspend. Cut that off with a rule you follow every time.

- Withdraw first: The moment you hit your profit target, withdraw before the next bet.

- Lock a percentage away: Set a fixed split, for example 50 percent of profits to savings, 50 percent stays as play money.

- No budget raise from wins: Your monthly budget stays the same. A win does not change your limit.

How to Handle Losses Responsibly: Stop-Loss and Reset Protocols

Losses trigger chasing. Your rules must kick in before you feel the urge.

- Session stop-loss: Pick a hard number. When you hit it, you stop. No reload.

- Daily stop-loss: If you play multiple sessions, cap total daily loss.

- Two-strike rule: If you hit stop-loss twice in a week, you take a full week off.

- Reset protocol: After any limit break, pause for 24 hours, remove payment methods again, and lower next month’s budget.

Game Choice Matters: Volatility, House Edge, and Bankroll Drain

Low vs. high volatility: swings feel personal, but they are math

Volatility is how wide your results swing.

- Low volatility pays smaller wins more often. Your bankroll moves slower.

- High volatility pays less often, but wins can be large. Your bankroll can drop fast before any win shows up.

High volatility creates long losing streaks. That does not mean you play “wrong.” It means your budget must cover variance.

If you cannot watch 20 to 50 straight losing bets without chasing, avoid high volatility games.

Game speed drives spending: faster games drain budgets faster

Speed matters as much as odds. More rounds per hour means more money exposed to the house edge.

- Slots run fast. Autoplay and turbo spins increase rounds per hour. Your losses can stack before you notice.

- Table games run slower. You make fewer bets per hour. Your budget lasts longer at the same bet size.

- Sports betting runs slowest. Fewer decision points, but bigger stakes per bet can cancel that benefit.

Set a pace rule. No autoplay. No turbo. One bet per hand, one spin at a time.

Promotion and bonus reality check: wagering can force overspending

Bonuses often come with wagering requirements. That requirement pushes you to bet more total money than you planned.

- Example: $100 bonus with 35x wagering means you must place $3,500 in bets before you can withdraw bonus-linked funds.

- Game restrictions matter. Slots may count 100%. Table games may count 10% or 0%.

- Max bet rules matter. Breaking them can void winnings.

Use one rule. If clearing the bonus needs more than your planned weekly action, skip it.

If a bonus makes you raise stakes, extend sessions, or reload, it is not “free.” It is a spending trigger.

RTP and house edge: what they mean for your budget in dollars

House edge is your long-run cost per dollar wagered. RTP is the flip side.

Use a simple estimate: Expected loss = total amount wagered x house edge.

| Game type (typical) | House edge (typical) | If you wager $1,000 total |

|---|---|---|

| High RTP blackjack (with correct play) | ~0.5% to 1.5% | ~$5 to $15 expected loss |

| European roulette | 2.7% | ~$27 expected loss |

| American roulette | 5.26% | ~$52.60 expected loss |

| Typical online slots | ~3% to 10%+ | ~$30 to $100+ expected loss |

This does not predict your next session. It tells you what your budget fights over time. The more you cycle through bets, the more that edge shows up.

Choose games to match your budget, not the other way around

- If your budget is tight, pick slower games and lower house edge.

- If you play slots, pick lower volatility titles, lower stakes, and limit spins per session.

- If you play roulette, avoid American wheels when you have a choice.

- If you chase big jackpots, cap exposure. Small stake, short session, hard stop-loss.

Build your plan around the game’s drain rate. Then lock it in with deposit limits and other responsible gambling tools.

Examples of Budgets That Work (and Budgets That Don’t)

Example 1: Casual casino player with a fixed monthly entertainment budget

You treat gambling like movies or dining out. You set a monthly cap you can afford to lose.

- Monthly cap: $100 to $300, based on your entertainment budget, not your income.

- Session plan: Split into 2 to 4 sessions. Example, $200 per month becomes four $50 sessions.

- Stop-loss: 100% of the session stake. If the $50 is gone, you stop.

- Win rule: Cash out a set share of profit. Example, lock 50% of winnings and only play with the rest.

- Tool: Set a deposit limit that matches the monthly cap. Do not raise it mid-month.

This works because it fits real cash flow and sets a clear end point per session.

Example 2: Sports bettor using units and weekly caps

Units stop you from sizing bets based on emotion. Weekly caps stop you from chasing after a bad run.

- Bankroll: A fixed amount you can lose. Example, $500 for the season.

- Unit size: 1% to 2% of bankroll. Example, $5 to $10 units on a $500 bankroll.

- Bet size rule: Most bets stay at 1 unit. Larger bets stay rare and capped, example 2 units max.

- Weekly cap: 5% to 10% of bankroll. Example, $25 to $50 per week on a $500 bankroll.

- Loss rule: If you hit the weekly cap, you stop betting until next week.

| Bankroll | 1 unit (1%) | 1 unit (2%) | Weekly cap (5%) | Weekly cap (10%) |

|---|---|---|---|---|

| $250 | $2.50 | $5 | $12.50 | $25 |

| $500 | $5 | $10 | $25 | $50 |

| $1,000 | $10 | $20 | $50 | $100 |

A 2024 NerdWallet survey reported average self-reported annual gambling spend of $3,284. If your plan drifts toward that level without intent, tighten your caps and tracking.

Example 3: Vacation gambling plan with a hard stop and cash-only rule

Vacations make overspending easy. You need friction and a hard ceiling.

- Total trip stake: A fixed amount for the whole trip. Example, $300 for three nights.

- Cash-only: Withdraw once. Leave cards out of the casino.

- Daily envelope: Split the cash. Example, three envelopes of $100.

- Session cap: Set a per-session limit inside the day. Example, two sessions of $50.

- Hard stop: When the cash is gone, you stop for the trip. No ATM, no room charge.

This works because you cannot redeposit. You cannot reload without breaking a rule you set in advance.

Red-flag budget: relying on credit, overdraft, or bill money

These budgets fail because the money is not yours to lose.

- Credit cards: You turn losses into long-term debt and interest.

- Overdraft: You add bank fees on top of losses.

- Bill money: You create a shortfall you must cover later, often by gambling more.

- “I will win it back” planning: You base your budget on results you cannot control.

If any of these show up, treat it as a warning sign. Use responsible gambling tools to add hard limits fast.

How to right-size an unrealistic plan without quitting entirely

- Start with a smaller cap: Cut your current spend by 50% for 30 days. Track every deposit and cash withdrawal.

- Shorten sessions: Keep the same monthly cap, but reduce time per session. Fewer decisions reduces tilt.

- Lower stakes first: Drop bet size before you change games. You reduce losses without needing willpower.

- Add a cooling-off rule: After any session loss, wait 24 hours before you play again.

- Use a two-limit setup: Set a deposit limit and a loss limit. Make both match your plan.

- Remove reload paths: Delete saved cards, block gambling payments, avoid ATMs during sessions.

Your budget works when it matches your cash flow, your game’s drain rate, and your ability to stop. If it depends on exceptions, it will break.

Warning Signs Your Gambling Budget Isn’t Working

Behavioral signs

- You hide play. You clear browser history, turn off notifications, or avoid talking about gambling.

- You get irritable when you cannot play. You snap at people, lose focus, or feel restless until you place a bet.

- You chase losses. You raise stakes, extend sessions, or break your stop rules to “get even.”

- You lie about losses. You downplay amounts, change the story, or avoid showing statements.

- You break your own limits. You “make an exception” more than once. Your rules stop meaning anything.

Financial signs

- You miss bills or pay late. Rent, utilities, phone, or credit cards slip because gambling took the cash.

- You borrow to keep playing. You use friends, family, payday loans, credit cards, or cash advances.

- You sell items to fund deposits. You pawn, resell, or trade things to refill your bankroll.

- You run overdrafts or rack up fees. You hit negative balances, trigger NSF charges, or rely on “float” until payday.

- Your gambling spend stops matching your plan. Your monthly total climbs while your income stays flat. That gap becomes debt.

Emotional signs

- You gamble to escape. You play to avoid stress, conflict, boredom, or loneliness.

- You feel anxiety around money and play anyway. You deposit while worried, then feel worse after the session.

- You use gambling to change your mood. You start low, then keep playing to hold onto relief or excitement.

- You feel depressed after losses. You withdraw, lose sleep, or struggle to do normal tasks.

Escalation pattern

- Your deposits increase to feel the same thrill. You move from small reloads to larger top-ups because small bets stop working.

- Your bet sizes creep up. You “round up” stakes, add parlays, or jump limits to speed up recovery.

- Your sessions get longer. You plan for a short session, then keep extending it until your balance forces you out.

- You change games for bigger swings. You switch to higher volatility slots, higher limits, or faster betting formats.

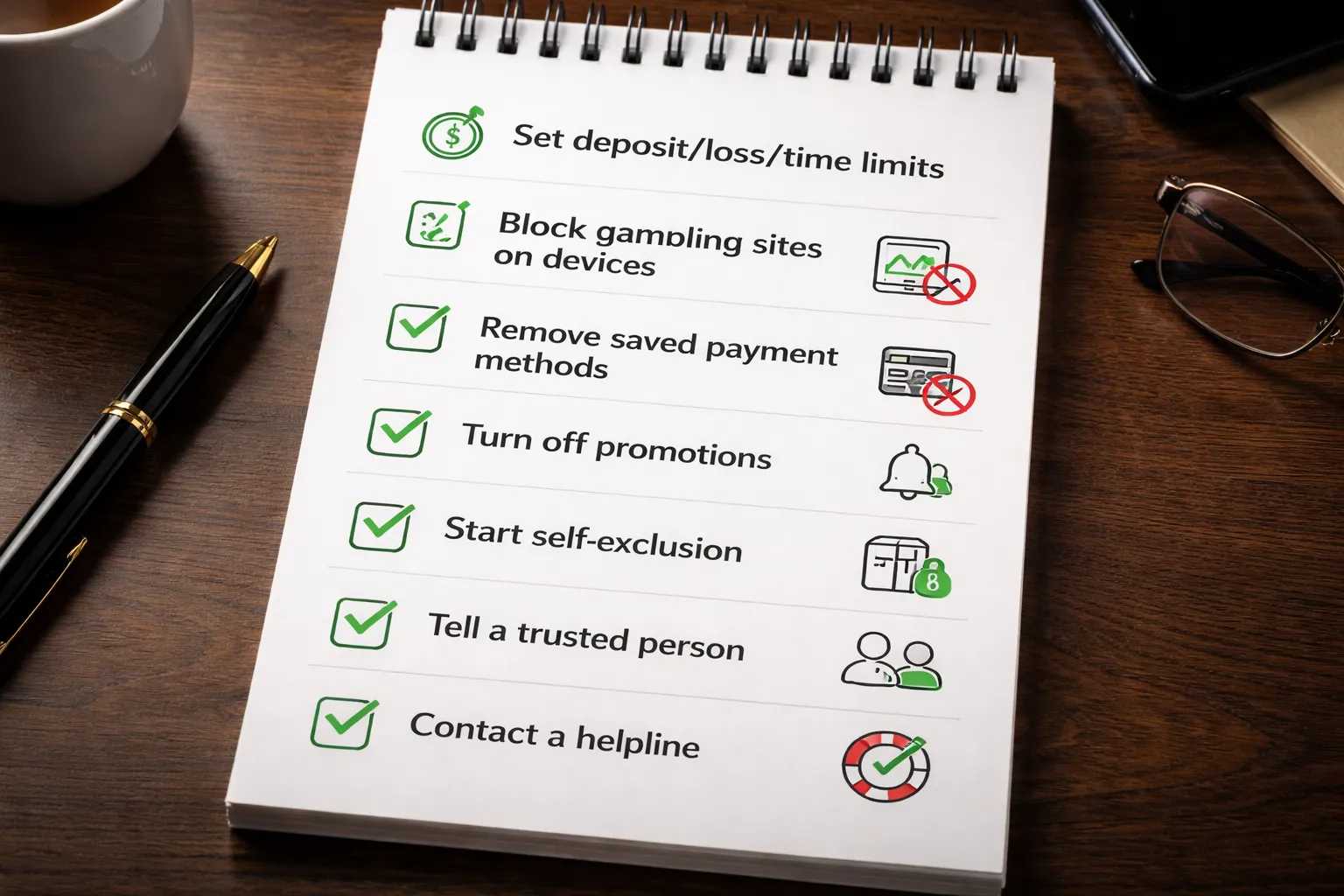

What to do immediately if you notice these signs

- Stop play for 72 hours. No deposits, no bets, no “small” sessions. This breaks the loop and shows you how strong the pull is.

- Lock down access. Turn on deposit limits and loss limits, then add a cooling-off or self-exclusion option. Use your operator settings first.

- Remove fast money. Delete saved cards, remove Apple Pay or Google Pay, and block gambling merchant codes with your bank if available.

- Write a one-page money snapshot. List cash on hand, bills due in 30 days, minimum debt payments, and recent gambling spend. Use real statements.

- Tell one person the number. Share your weekly or monthly gambling cap and your last 30 days of losses. Secrecy keeps the leak open.

- Set a hard rule for any future play. If you cannot follow it, you do not gamble. Example, one session per week, fixed amount, no reloads.

- Use support tools now. See responsible gambling tools and set them before you feel tempted again.

Responsible Gambling and Getting Help (If You Need It)

Practical harm-reduction steps you can take today

- Set limits before you play. Deposit limit, loss limit, session time limit. Set all three. Do it on every site and app you use.

- Block access on your devices. Use gambling site blockers on your phone and laptop. Set a passcode you do not know, give it to a trusted person.

- Remove fast funding. Delete saved cards, unlink Apple Pay and Google Pay, remove PayPal where possible. Turn off “one tap” deposits.

- Turn off marketing. Unsubscribe from promo emails and texts. Disable push notifications in your phone settings.

- Stop chasing mechanics. No reloads. No “one last bet.” No increases after a loss.

- Put friction in your cash flow. Keep gambling money in a separate account with no overdraft. Do not carry that card day to day.

- Track one number. Net loss for the month. Not wins. Not turnover. Loss.

When to take a complete break vs. reduce spend

Reduce spend only works when you still control your actions. If you keep breaking rules, you need a full stop.

- Take a complete break if: you borrow to gamble, you use rent or bill money, you hide losses, you chase, you feel panic when you try to stop, you keep raising limits, you gamble when you planned not to, you gamble to fix stress or mood.

- Reduce spend only if: you can follow preset limits for at least 30 days, you stop when the session ends, you do not reload, you do not try to win back losses.

If you choose a break, set a clear length. Start with 30 days. Add barriers, not willpower. Self-exclude. Block sites. Tell one person.

How self-exclusion works and what it does (and doesn’t) prevent

Self-exclusion is a formal lock. You ask an operator, a state program, or a national program to block your access for a set time.

- What it does: blocks you from logging in, wagering, or receiving many promos on the sites covered. It can stop new account signups with the same details. It creates a clear rule you cannot “talk your way out of” in a weak moment.

- What it does not do: stop you from using unlicensed sites, using someone else’s account, or finding new platforms not covered by that program. It also does not fix debt, anxiety, or relationship damage by itself.

- What to do with it: combine it with device blocks, funding limits, and telling one person. Treat it as one layer in your safety system.

For a step-by-step breakdown, read our guide on how online casino self-exclusion works.

Talking to someone, preparing for a difficult conversation

You need one person who will not gamble with you, lend you money, or keep secrets for you. Pick someone steady.

- Prepare two numbers. Your monthly cap, and your net loss in the last 30 days.

- Bring evidence. A bank statement or a transaction list. One page. Real dates. Real amounts.

- Use direct lines. “I am not controlling it.” “I need help sticking to a limit.” “I need you to hold the passcode.”

- Ask for one action. Not a speech. Not a promise. One action such as holding your blockers, checking in weekly, or helping you self-exclude.

- Set a money boundary. Tell them you do not want loans. Loans keep gambling alive.

Finding local support resources and professional help options

Help works best when it is easy to reach and specific. Use more than one option.

- National helplines. Search “problem gambling helpline” plus your country or state. Many offer phone, text, and chat.

- Counseling. Look for therapists who list gambling disorder, addiction counseling, or CBT. Ask if they have direct experience with gambling.

- Support groups. Gamblers Anonymous and other peer groups run local and online meetings. You get structure and accountability fast.

- Financial support. A nonprofit credit counselor can help you build a payment plan and remove access to credit triggers.

- Medical support. If you have severe anxiety, depression, or thoughts of self-harm, contact emergency services or a crisis line now. Treat this as urgent.

Set one appointment today. Put it on your calendar. Tell your chosen person the date and time.

FAQ

What is a gambling budget?

Your gambling budget is a fixed amount you can lose without missing bills, debt payments, or savings. Treat it as entertainment spend. Set it before you play. When it is gone, you stop.

How much should I budget for gambling?

Use your disposable income only. Start low. Many guides suggest 1 to 5 percent of disposable income, not total income. If you have debt balances, missed bills, or no emergency fund, set it to zero until you stabilize.

How do I calculate disposable income fast?

Add your monthly take-home pay. Subtract fixed costs, bills, debt minimums, groceries, transport, and required savings. What remains is disposable income. If the number is negative, you cannot afford gambling this month.

How do I make sure I stick to the budget?

Use hard limits. Set deposit limits inside the app. Use one separate card or prepaid balance. Turn off saved payment methods. Track every deposit and withdrawal. Add a stop time. Tell one person your monthly limit and results.

Should I chase losses to get back to even?

No. Chasing losses breaks your limit and raises your risk of bigger losses fast. Treat a loss as the cost of the session. Stop when you hit your loss cap. Do not increase stakes to recover.

Should I raise my budget after a win?

No. Wins do not change affordability. Keep the same monthly limit. If you withdraw, move money out of your gambling account the same day. If you keep playing, you risk giving the win back.

What limits should I set inside gambling apps?

Set a deposit limit, a loss limit, and a time limit. Use cool-off periods if you struggle to stop. If limits fail, use self-exclusion. See responsible gambling tools.

What if I keep breaking my budget?

Treat it as a warning sign. Lower your limit to zero for 30 days. Block gambling transactions with your bank if possible. Remove apps. Ask someone to hold you accountable. If you feel out of control, choose self-exclusion and get professional help.

How much do people say they spend on gambling?

A 2024 NerdWallet survey on sports betting found respondents reported average spending of $3,284. Use this as a reality check, not a target. Your safe number depends on your bills, debt, and savings, not the average.

Conclusion

Conclusion

A gambling budget works when you treat it like a bill. You set the number first. You follow it every time.

Use the $3,284 average from the 2024 NerdWallet survey as a warning sign. Your budget should match your income, your debt, and your savings goals. If the math does not work, your budget is $0.

- Pick one monthly limit. Keep it small enough that missing it changes nothing.

- Split it into session limits. Stop when the session money is gone.

- Separate the funds. Use a prepaid card or a dedicated account. Never use credit.

- Track every deposit. If you cannot track it, you cannot control it.

- Set a hard stop. Use site limits, remove apps, and block deposits when you hit your cap.

Your final step is simple. Put your limit in writing. Set it inside the site. If you keep breaking your limits, use self-exclusion and get support.

-

Online Casino Licensing Explained: Authorities, Licenses & How to Check One

5 months ago -

Problem Gambling Signs: How to Recognize the Warning Flags Early

5 months ago -

Responsible Gambling Tools Explained: Deposit Limits, Self-Exclusion & More

5 months ago -

Online Casino Self-Exclusion: How It Works and What Happens Next

5 months ago -

Online Casino Customer Support: What to Look For (Live Chat, Email, Response Times)

5 months ago

-

- Low vs. high volatility: swings feel personal, but they are math

- Game speed drives spending: faster games drain budgets faster

- Promotion and bonus reality check: wagering can force overspending

- RTP and house edge: what they mean for your budget in dollars

- Choose games to match your budget, not the other way around

-

- Example 1: Casual casino player with a fixed monthly entertainment budget

- Example 2: Sports bettor using units and weekly caps

- Example 3: Vacation gambling plan with a hard stop and cash-only rule

- Red-flag budget: relying on credit, overdraft, or bill money

- How to right-size an unrealistic plan without quitting entirely

-

- What is a gambling budget?

- How much should I budget for gambling?

- How do I calculate disposable income fast?

- How do I make sure I stick to the budget?

- Should I chase losses to get back to even?

- Should I raise my budget after a win?

- What limits should I set inside gambling apps?

- What if I keep breaking my budget?

- How much do people say they spend on gambling?

-

- Low vs. high volatility: swings feel personal, but they are math

- Game speed drives spending: faster games drain budgets faster

- Promotion and bonus reality check: wagering can force overspending

- RTP and house edge: what they mean for your budget in dollars

- Choose games to match your budget, not the other way around

-

- Example 1: Casual casino player with a fixed monthly entertainment budget

- Example 2: Sports bettor using units and weekly caps

- Example 3: Vacation gambling plan with a hard stop and cash-only rule

- Red-flag budget: relying on credit, overdraft, or bill money

- How to right-size an unrealistic plan without quitting entirely

-

- What is a gambling budget?

- How much should I budget for gambling?

- How do I calculate disposable income fast?

- How do I make sure I stick to the budget?

- Should I chase losses to get back to even?

- Should I raise my budget after a win?

- What limits should I set inside gambling apps?

- What if I keep breaking my budget?

- How much do people say they spend on gambling?

-

Reload Bonus Explained: What It Is and When It’s Worth Claiming

3 months ago -

Online Casino Licensing Explained: Authorities, Licenses & How to Check One

5 months ago -

Best Live Dealer Casinos: Where to Play Live Blackjack, Roulette & More

5 months ago -

Best Online Casinos for High Rollers: VIP Perks, High Limits & Exclusive Bonuses

5 months ago -

Fast Payout Online Casinos: Best Sites for Quick Withdrawals

5 months ago

-

Online Casino Licensing Explained: Authorities, Licenses & How to Check One

5 months ago -

Are Online Casinos Legal? Complete Guide by State & Country

5 months ago -

Casino VIP & Loyalty Programs Explained: Points, Tiers, Rewards & Rakeback

5 months ago -

Online Casino Fairness Explained: RNG, RTP, House Edge & Provably Fair

5 months ago -

Free Spins Bonus Explained: How Free Spins Work at Online Casinos

5 months ago